Feed Aggregator Page 596

Rendered on Fri, 13 Jan 2017 16:30:09 GMT

Rendered on Fri, 13 Jan 2017 16:30:09 GMT

via Motley Fool Headlines by on Fri, 13 Jan 2017 16:11:00 GMT

via Motley Fool Headlines by on Fri, 13 Jan 2017 16:05:00 GMT

via Motley Fool Headlines by on Fri, 13 Jan 2017 16:04:00 GMT

via by Tyler Durden on Fri, 13 Jan 2017 15:55:00 GMT

In late December, we explained why of all Trump economic proposals , the "border tax adjustment", while most controversial, could have the biggest impact on US assets.

As a quick refresher, the proposal would tax US imports at the corporate income tax rate, while exempting income earned from exports from any taxation. The reform would closely mirror tax border adjustments in economies with consumption-based VAT tax systems. If enacted, Deutsche Bank predicted that the plan would be especially bullish for the US dollar, sending it higher by as much as 15%. What’s more, it would have a transformational impact on the US trade relationship with the rest of the world. Consider the below:

In other words, should the "border tax proposal" pass, it would not only send inflation soaring, while eliminating the US trade deficit - a long-time pet peeve of Trump - it would also be the trade-equivalent of a 15% USD devaluation, even as it leads to an offsetting surge in the actual value of the dollar.

To be sure, the "should it pass" part is a significant wildcard. As Goldman wrote in a note yesterday, explaining "what policy changes is the equity market expecting", Goldman said that "on the tax side, the equity market appears to expect corporate tax cuts, but the evidence that a switch to a border-adjusted tax is even partially priced is only mixed."

A reason for that within the GOP ranks, a fight has emerged - funded by powerful Koch interests - against the border tax proposal, as it would cripple non-export driven businesses such as importers, apparel makers, big retailers, and various core Koch businesses as described recently by the FT.

So while the passage of the controversial Border Tax Adjustment is far from assured, overnight Credit Suisse released an analysis which analyzed the various winner and losers from the array of proposed Trump Tax Reforms, among which companies impacted by the Border Adjustment.

While the Swiss bank hedges early, noting that it is still "too early to determine winners/losers as new information is surfacing daily…and the legislative process needs to run its course this year" and that "reforms (complexity) could impact the effective tax rate, cash taxes, and/or possibly COGS (border adjustments)", it nonetheless does quantify who the various winners and losers from the BTA would be, which it frams as follows:

Here is Credit Suisse' answer:

Potential Winners

Potential Losers

CS then looks at which specific companies could find border adjustments a potential positive, among which:

3M (MMM) Analyst Meeting – 2017 Outlook: There's three points on the border adjustment portion.

General Electric (GE) Investor Meeting – December, 2017: We're a big exporter and not a big importer.

And then, a potential negative:

The bank next points out that companies already “manufacturing” (at least partially) in the U.S. could be in a better position under tax reforms:

A factor here would be the domestic manufacturing deduction (DMD):

On the other hand, companies with high levels of foreign earnings and very low foreign tax rates, are at increased risk:

Profit shifting

Finally, here is a practical example of how BTA might work in real life:

via Motley Fool Headlines by on Fri, 13 Jan 2017 15:48:00 GMT

via Motley Fool Headlines by on Fri, 13 Jan 2017 15:44:00 GMT

via Motley Fool Headlines by on Fri, 13 Jan 2017 15:41:00 GMT

via by Tyler Durden on Fri, 13 Jan 2017 15:34:28 GMT

Over the year, Deutsche Bank has been accused - and found guilty - of doing many illegal things (and paid handsomely for it, both in terms of penalties as well as sacked CEOs), but what happened yesterday was new.

As we observed yesterday morning, as part of his latest attack on currency speculators, Erdogan compared FX traders to terrorists, saying that "terrorists with dollars and with weapons have no difference." Furthermore, on Thursday the government friendly daily Yeni Safak reported that Deutsche Bank and other German institutions were attempting “economic terror” against Turkey by recalling loans to companies before their their due dates.

The German lender was not happy, and on Friday Deutsche Bank’s Turkish unit rejected claims that it’s plotting to undermine the economy, and said it’s “unacceptable” for the lender’s name to be associated with terrorism.

“Claims in the story about calling loans before their maturity and conducting operations in coordination with other institutions are totally groundless,” the bank’s Istanbul-based business said in an e-mailed statement Friday quoted by Bloomberg.

Like many other failing regimes, most notably Venezuela, Erdogan and his aides often invoke a conspiracy against Turkey by outside powers when the lira declines, "saying other nations are jealous of the country’s economic growth under his leadership." On Thursday, Erdogan accused Turkey’s enemies of speculating in the lira and again called on Turks to “thwart these games” by selling their holdings in other currencies.

Meanwhile, the one thing that could prop up the crashing currency, a rate hike, has been virtually proihibted by Erdogan who has warned that any such action by the central bank will be rejected by his administration. Erdogan is hoping to boost the lagging economy with cheap loans, however in the process it has sent the currency plunging.

Thursday was not the first time that Deutsche Bank has been singled out by the Turkish press. In January 2014, the German lender denied local reports that it deliberately drove down shares of a Turkish state-run lender that had been implicated in a corruption scandal. Deutsche Bank said most of the shares it processed in that episode were owned by its clients, and it wasn’t trading sufficient volumes to affect the company’s share price. More recently, the Frankfurt-based institution figured in a different way in government rhetoric.

In an amusing interlude, last September, when Deutsche Bank's shares were plunging, amid capital concerns, Yigit Bulut, a chief adviser to Erdogan, said Turkey should consider buying Deutsche Bank.

“Some very good companies in the EU are going to fall into trouble and we need to be ready to buy a controlling stake in them,” Bulut wrote on Twitter. "Wouldn’t you be happy to make Germany’s biggest bank into a Turkish Bank!!"

As Bloomberg adds, Bulut also criticized Germany’s flagship carrier, Deutsche Lufthansa AG, soon after his appointment in 2013. He said the airline was behind anti-government protests that began in Istanbul’s Gezi Park that summer, because its position in Europe was threatened by plans to build a new airport in Istanbul.

Deutsche Bank, which has been in Turkey since 1987, employs 143 people at its Turkish unit. In the next TRY crisis, it is a distinct possibility many if not all could be arrested on allegations they are conspiring to take down Erdogan, whose authoritarian ways have been mostly ignored by the country's western friends and allies.

via Motley Fool Headlines by on Fri, 13 Jan 2017 15:32:00 GMT

via Motley Fool Headlines by on Fri, 13 Jan 2017 15:31:00 GMT

via by Tyler Durden on Fri, 13 Jan 2017 15:20:00 GMT

Submitted by Charles Hugh-Smith via OfTwoMinds blog,

These eight forces are structural, and cannot be erased by tax cuts or policy tweaks.

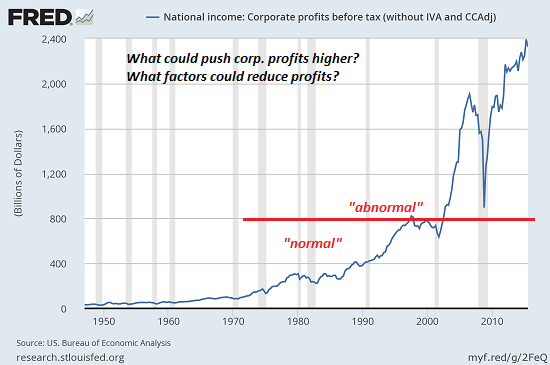

If there is any economic assumption that goes unquestioned, it's the notion that profits will remain robust for the foreseeable future. This assumption ignores the tidal forces that are now flowing against profits.

Any discussion of corporate profits must start by noting the astonishing rise in U.S. corporate profits since the heyday of the late 1990s dot-com boom. From $800 billion to $2.4 trillion in a few years is not just extraordinary--it's unprecedented.

Yet rather than wonder if this incredible spike higher is temporary, the financial media assumes nosebleed-lebvel profits are a new and wonderful plateau that can only move higher in the future.

This confidence ignores the systemic tidal forces working against profits.

1. Higher costs of capital. Another blithe assumption is that capital will cost almost nothing to borrow, as far as the eye can see, and that the demand for low-yield corporate debt will remain insatiable.

The yield on bonds is rising in important markets, and while many observers reckon rates will soon return to zero (or less than zero), others see the potential for a trend change from declining rates (a 45 year trend) to rising rates.

Rising borrowing costs pressure profits.

2. Rising wages and labor overhead. Even if wages remain stagnant, the overhead costs of labor--healthcare, workers compensation, pensions, etc.--are increasing for structural reasons. Factor in global pressure to raise minimum wages and competition for the most productive labor/skillsets, and the cost of labor is rising on multiple fronts. Rising labor costs pressure profits.

3. Urbanization. An unprecedented number of working-age people have migrated from largely self-sufficient rural economies to high-cost urban economies that require much more cash income. As Immanuel Wallerstein has observed, urbanization pushes wages higher, regardless of the era or the nation experiencing the urbanization.

While cheerleaders focus on the higher income of these tens of millions of new urban dwellers, and on the potential for corporations to sell them more products and banks to lend them money, low-wage workers spend the vast majority of their income on rent, food and transport. Beyond these essentials, opportunities to earn fat margins selling to the urban poor are scarce.

4. Expanding competition and market saturation. Have you noticed how companies are getting into everyone else's business? You see all sorts of non-building supplies being sold in Home Depot, for example. With sales stagnant in the developed world and in emerging markets hit by recession or currency devaluations, expanding into established markets is seen as one of the few ways to grow sales and profits.

There is an upper limit to this trend, of course. McDonalds can grow sales by opening branches in Walmarts, and Starbucks can expand sales by opening a shop in every Target, but we're clearly reaching saturation on retail outlets everywhere. As for online sales--everybody's trying to expand their online sales, but often at the cost of lost bricks-and-mortar store sales.

5. Trade wars and de-globalization. Profits have soared for corporations that have mastered long global supply chains that serve a wide range of regional markets. Any disruption in these long supply chains due to geopolitical tensions, trade disputes or domestic pressures to relocate production back in the home country will increase costs incrementally.

6. Higher taxes. The rotation from relying of monetary expansion (quantitative easing, bond purchases, etc.) for growth to fiscal expansion (borrow and spend for infrastructure, etc.) will eventually require higher taxes on labor and capital to fund the higher fiscal spending. Higher taxes pressure profits.

7. Debt saturation. Debt has been rising across the board for the eight years of "recovery," and a slowing of debt expansion means there will be less money available to spend on goods and services. Slowing debt and slowing sales pressure profits.

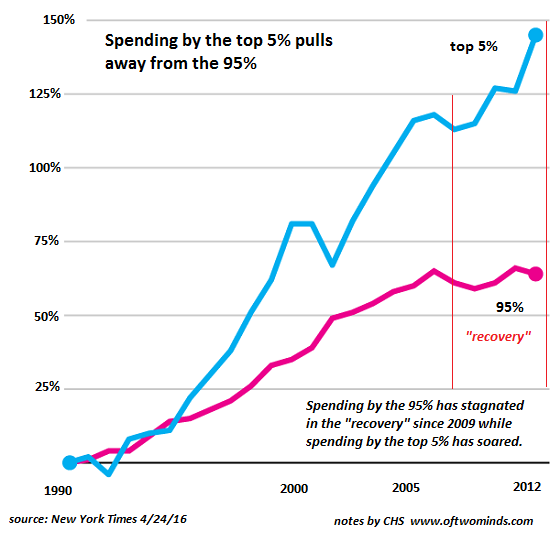

8. Decline of the wealth effect. Most of the wealth effect--the psychological sense of feeling wealthier and thus more prone to borrow and spend--is concentrated in the top 5% of households that own most of the assets that have bubble higher over the past eight years. (A lesser wealth effect has trickled down the next 15%.)

The wealth effect's influence on consumption is readily visible in this chart that shows spending by the top 5% has pulled away from the spending of the bottom 95%.

Should the bubblicious asset classes that have experienced strong gains--stocks, bonds and housing-- suddenly encounter turbulence or an actual downdraft (gasp), the wealth effect will quickly wear thin, potentially impacting the biggest spenders that have been driving corporate profits.

These eight forces are structural, and cannot be erased by tax cuts or policy tweaks.

via Motley Fool Headlines by on Fri, 13 Jan 2017 15:13:00 GMT

via by Tyler Durden on Fri, 13 Jan 2017 15:08:21 GMT

After surging to 12-year highs in December, following Trump's election victory, UMich consumer sentiment faded in January and missed expectations (98.1 vs 98.5 exp). While inflation outlooks picked up modestly off record lows, economic 'expectations' - hope - dipped from 89.5 to 88.9 as the Trump Bump appears to have stalled.

While not quite as big a drop as Bloomberg confidence data, it appears Trumphoria is fading...

Even as inflation outlooks bounce off record lows...

On the bright side, survey respondents improved their view of it "being a good time to buy" Household Items, Homes, and Vehicles.

via Motley Fool Headlines by on Fri, 13 Jan 2017 15:07:00 GMT

via Motley Fool Headlines by on Fri, 13 Jan 2017 15:02:00 GMT

via by Tyler Durden on Fri, 13 Jan 2017 14:53:06 GMT

While one can argue that both JPM and Bank of America posted results that were ok, with some aspects doing better than expected offset by weakness elsewhere, even if moments ago JPM stock just hit an all time high, there was little to redeem the report from the scandal-ridden largest mortgage lender in America, Wells Fargo. Not only did the company miss revenues significantly, reported $21.6bn in Q4 topline, nearly $1 bn below the $22.4bn consensus, but it had to reach deep into its non-GAAP adjustment bag to convert the $0.96 EPS miss into a $1.03 EPS beat (net of "accounting effect"), but the details of its core business were, well, deplorable, which perhaps was to be expected following the recent drop in new credit card and bank account growth, following last year's fake account scandal.

Incidentally, Wells Fargo reported its latest customer metrics alongside 4Q earnings, and in December the bank said that the retail public continued to shy away, as new checking accounts plunged 40%Y/Y while new credit card applications tumbled 43%. On the other hand, deposit balances debit card transactions continued growing which probably is not a good sign, if only for the Keynesians in the administration: it means that consumers are saving.

But back to Wells results, which revealed that in Q4, the bank's ROE, one of Buffett's favorite indicators, fell to 10.94%. which was the lowest quarterly level posted in years accordint to the WSJ. "While the return had been grinding lower for some time, largely due to the declining interest-rate environment, the fourth quarter also marked the first, full reporting period since the bank’s sales-tactics scandal erupted in September."

More troubling however, was that in Q4, Wells overall profit fell to $5.27 billion, or 96 cents a share (excluding the various non-GAAP addbacks), down from $5.58 billion, or EPS of $1 in Q4 2015.

So back to Wells Fargo's retail banking business. Here the bank reported that while credit card outstandings rose 5% compared to $33.14 billion last quarter and jumped 8% from $34.04 billion in the year-earlier period, new accounts tumbled 52% to 319,000 from 667,000 last quarter and fell 47% from 597,355 in the year-earlier period, once again this is a reflection of the bank's ongoing legal scandals.

But it was the bank's bread and butter, mortgage lending, that was the biggest alarm because as a result of rising rates, Wells' residential mortgage applications and pipelines both tumbled, and after hitting multi-year highs in the third quarter when mortgage rates were likewise hugging multi-year lows, in Q4 Wells' mortgage applications plunged by $25bn from the prior quarter to $75bn, while the mortgage origination pipeline plunged by nearly half to just $30 billion, and just shy of all time lows recorded in late 2013 and 2014. Moynihan's explanation was redundant: "the pipeline is weaker because of fewer refi loans." This should not come as a surprise: just one month ago, Freddie Mac warned that as mortgage rates continue to surge, "expect mortgage activity to be significantly subdued in 2017."

Wells Fargo did not even have to wait that long, and as shown in the chart below, the biggest US mortgage lender is already suffering.

Expect even greater declines in the coming quarters should rates continue to rise.

via Motley Fool Headlines by on Fri, 13 Jan 2017 14:42:00 GMT

via Motley Fool Headlines by on Fri, 13 Jan 2017 14:36:00 GMT

via Motley Fool Headlines by on Fri, 13 Jan 2017 14:36:00 GMT

via Motley Fool Headlines by on Fri, 13 Jan 2017 14:36:00 GMT