Feed Aggregator Page 591

Rendered on Thu, 12 Jan 2017 23:00:08 GMT

Rendered on Thu, 12 Jan 2017 23:00:08 GMT

via by Tyler Durden on Thu, 12 Jan 2017 22:28:00 GMT

With just 8 days left until President Trump's inauguration ceremony in Washington D.C., a massive security force, including 7,500 Guardsmen and 3,000 police officers, is preparing for the worst as the event is expected to attract up to 750,000 protesters, some of whom have vowed to "paralyze the city." Certainly if the protester presence at the Senate confirmation hearings over the past two days is any indicator of what is to come, then next Friday should be an interesting evening.

More than three-dozen law enforcement agencies are working together on security and safety plans in anticipation, including the Capitol Police, FBI, Secret Service and National Guard.

Roughly 7,500 Guardsmen from across the country will come to Washington, along with about 3,000 police officers from various states, with the Secret Service taking the lead on security.

Essentially everybody involved already is rehearsing for the big weekend, which kicks off next Friday morning with the swearings-in on the Capitol’s West Front, followed by official events including the traditional parade on Pennsylvania Avenue to the White House and the inaugural balls.

The Joint Task Force -- National Capital Region -- 58th Presidential Inauguration has held several “table top” sessions in which agencies plot strategy over a large-scale, three-dimensional map.

“It’s a rehearsal, but in the military we call it a drill,” Navy Cmdr. Jonathan Blyth, the group’s spokesman, told FoxNews.com on Wednesday. “We’ve been preparing for this since the last inauguration. We’re focused to protecting and honoring a new commander in chief.”

Several anti-Trump groups are expected to host demonstrations on January 20th, including DisruptJ20 and RefuseFacism.org, with stated intentions to disrupt the inarguable ceremonies from the parade to the ball by using, among other tactics, human blockades to stop traffic, public transit and parties.

Several protest groups planning large-scale demonstrations have permits in place and have already held organizational meetings, among them the collaborative DisruptJ20.

“We’re planning a series of massive, direct actions that will shut down the inauguration ceremonies and any related celebrations,” the group says. “We’re also planning to paralyze the city.”

Organizers say they are targeting everything from the parade to the balls and plan to use blockades and protesters to stop traffic, public transit and parties.

The group RefuseFacism.org is planning a small-scale protest Saturday in the city’s McPherson Square, just blocks from the White House, that organizers hope will grow into larger inauguration-weekend protests.

The group burned U.S. flags this summer at the Democratic and Republican national conventions and this week tried to disrupt the Senate confirmation hearing for Alabama GOP Sen. Jeff Sessions to become Trump’s attorney general.

“I wouldn’t want to meet with [Trump], but I would say to him, ‘You’re a fascist. Your regime is illegitimate.’ And it must not be allowed to take power,” the group’s Carl Dix told Fox on Wednesday on Capitol Hill. Dix acknowledged the group doesn’t have a federal or city permit to protest but still intends to “stop the regime.”

Of course, the one pro-Trump organization that has registered for a demonstration permit is the now infamous "Bikers for Trump" group. And while we're sure they're only interested in peacefully supporting their candidate, we would highly recommend that the disaffected Hillary snowflakes stay far away from their reserved demonstration area.

Meanwhile, the protesting madness is expected to continue the day after inauguration with 200,000 women expected to join the Women’s March on Washington. The event is expected to draw the typical Hollywood crowd, including Amy Schumer, who was supposed to have left the country by now, and Scarlett Johansson.

We wish all the protesters the best of luck, we're sure your efforts will truly make a positive difference in the world.

via Motley Fool Headlines by on Thu, 12 Jan 2017 22:29:00 GMT

via Motley Fool Headlines by on Thu, 12 Jan 2017 22:24:00 GMT

via Motley Fool Headlines by on Thu, 12 Jan 2017 22:18:00 GMT

via Motley Fool Headlines by on Thu, 12 Jan 2017 22:09:00 GMT

via Motley Fool Headlines by on Thu, 12 Jan 2017 22:09:00 GMT

via by Tyler Durden on Thu, 12 Jan 2017 22:08:42 GMT

Ahead of a deluge of bank earnings reports starting tomorrow morning, which include JPMorgan, Wells Fargo and Bank of America, and all of which are "whispered" to come in above expectations, an ominous harbinger hit the newswires this afternoon when Reuters reported that Morgan Stanley not only laid off various senior investment bankers last week, just ahead of bonuses season, but also slashed investment banking bonuses by roughly 15% as a result of "a decline in revenue from dealmaking and capital raising across Wall Street."

While individual bankers bonuses fluctuated depending on performance and geographic region, many are said to have received a smaller paycheck for 2016. Furthermore Morgan Stanley, which remains a bulge bracket investment bank and ranked fourth in IB fees last year, also cut more than 20 MDs from its global investment banking division, roughly 5% of total.

While Morgan Stanley, like other major banks, typically lets go of the bottom 5% of its workforce at year-end to get rid of underperformers, the cuts to senior bankers were deeper than in years past, according to Reuters sources. Morgan Stanley also announced the promotion of managing directors on Thursday.

The layoffs will hardly come as a surprise as Wall Street banks have been shedding staff and curbing compensation for years to cut costs. They have also been losing top talent to boutique firms, which can pay a greater portion of compensation in cash. Further pressuring Wall Street's animal spirits, global investment banking fees across Wall Street declined 7% in 2016 to a three-year low, according to Thomson Reuters data.

While drops were recorded in most IB vertical, equity capital market fees, which declined 23 percent, were hit the most as a result of a drop off in initial public offerings. IPO activity in 2016 occurred at the lowest levels since 2009. M&A also slowed from record levels in 2015, with global deal volume falling 17%.

Ironically, despite being largely shunned by Wall Street ahead of the election, there is hope that banker compensation will rebound in 2017 thanks to Donald Trump, as a result of more active trading by retail investors, as well as a rebound in bond issuance (with the first 10 days of January already above $100 billion in IG issuance, an all time record) and other M&A and advisory activity.

via by Tyler Durden on Thu, 12 Jan 2017 21:55:00 GMT

Submitted by Lance Roberts via RealInvestmentAdvice.com,

Last week, I addressed the issue with consumer spending and the issue of consumer debt. To wit:

“Given the lack of income growth and rising costs of living, it is unlikely that Americans are actually saving more. The reality is consumers are likely saving less and may even be pushing a negative savings rate.

I know suggesting such a thing is ridiculous. However, the BEA calculates the saving rate as the difference between incomes and outlays as measured by their own assumptions for interest rates on debt, inflationary pressures on a presumed basket of goods and services and taxes. What it does not measure is what individuals are actually putting into a bank saving or investment account. In other words, the savings rate is an estimate of what is ‘likely’ to be saved each month.

However, as we can surmise, the reality for the majority of American’s is quite the opposite as the daily costs of maintaining the current standard of living absorbs any excess cash flow. This is why I repeatedly wrote early on that falling oil prices would not boost consumption and it didn’t.”

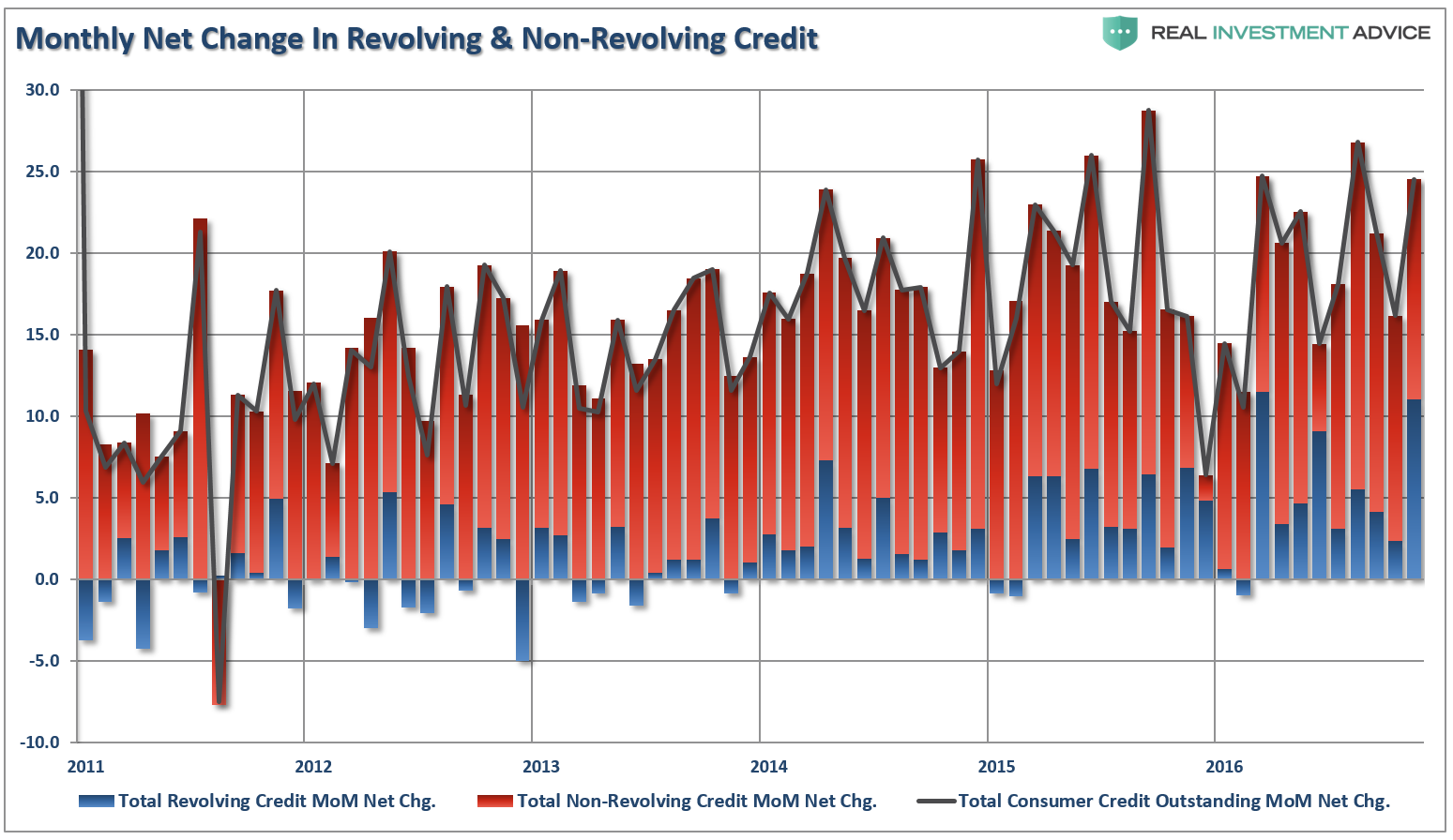

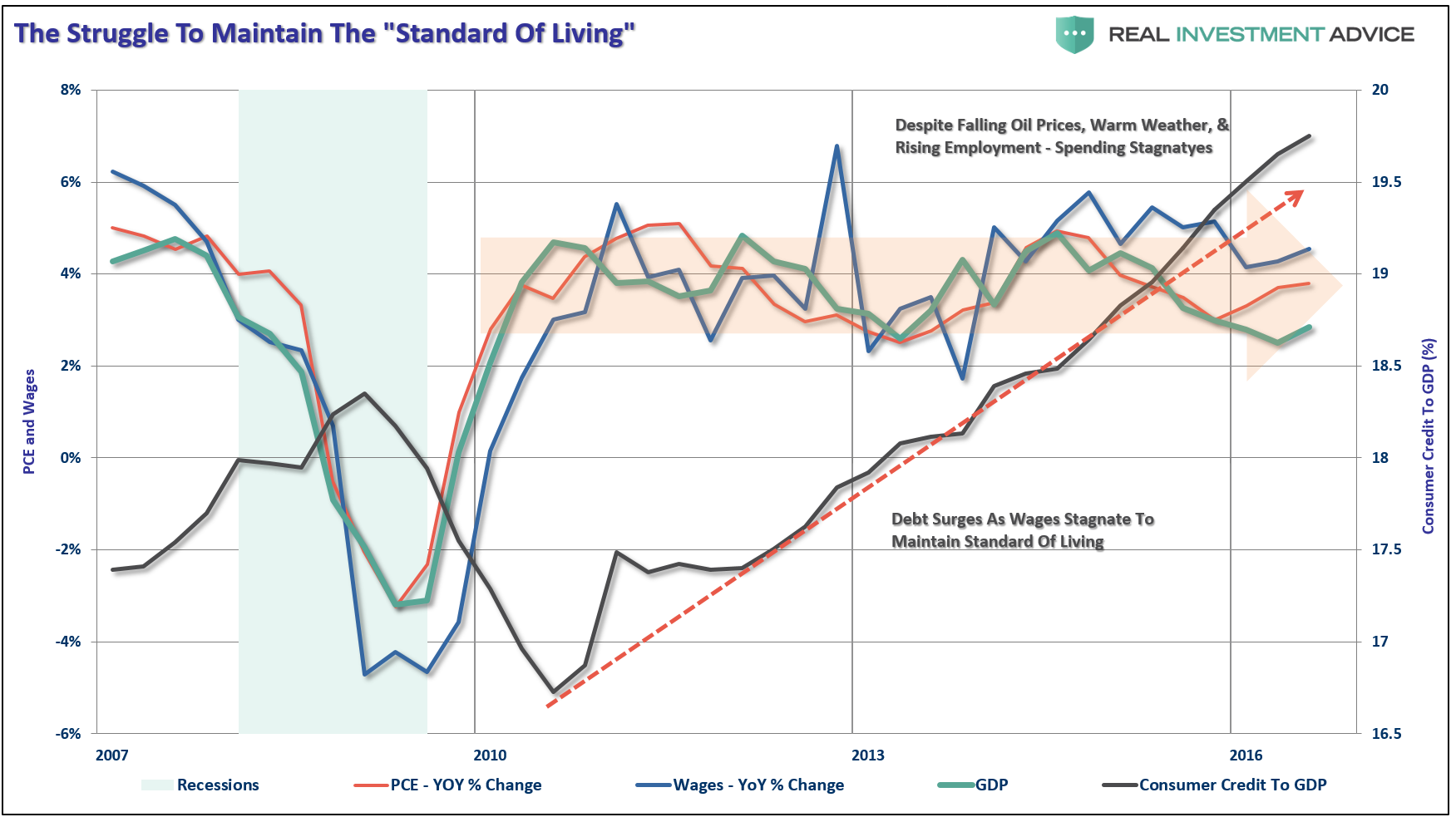

As shown in the chart below, consumer credit has surged in recent months and exploded in November rising $24.5 billion in the month alone.

More importantly, while consumer credit continued to# expand, PCE and Wages remain primarily stagnant.

“Here is another problem. While economists, media, and analysts wish to blame those ‘stingy consumers’ for not buying more stuff, the reality is the majority of American consumers have likely reached the limits of their ability to consume. This decline in economic growth over the past 30 years has kept the average American struggling to maintain their standard of living.”

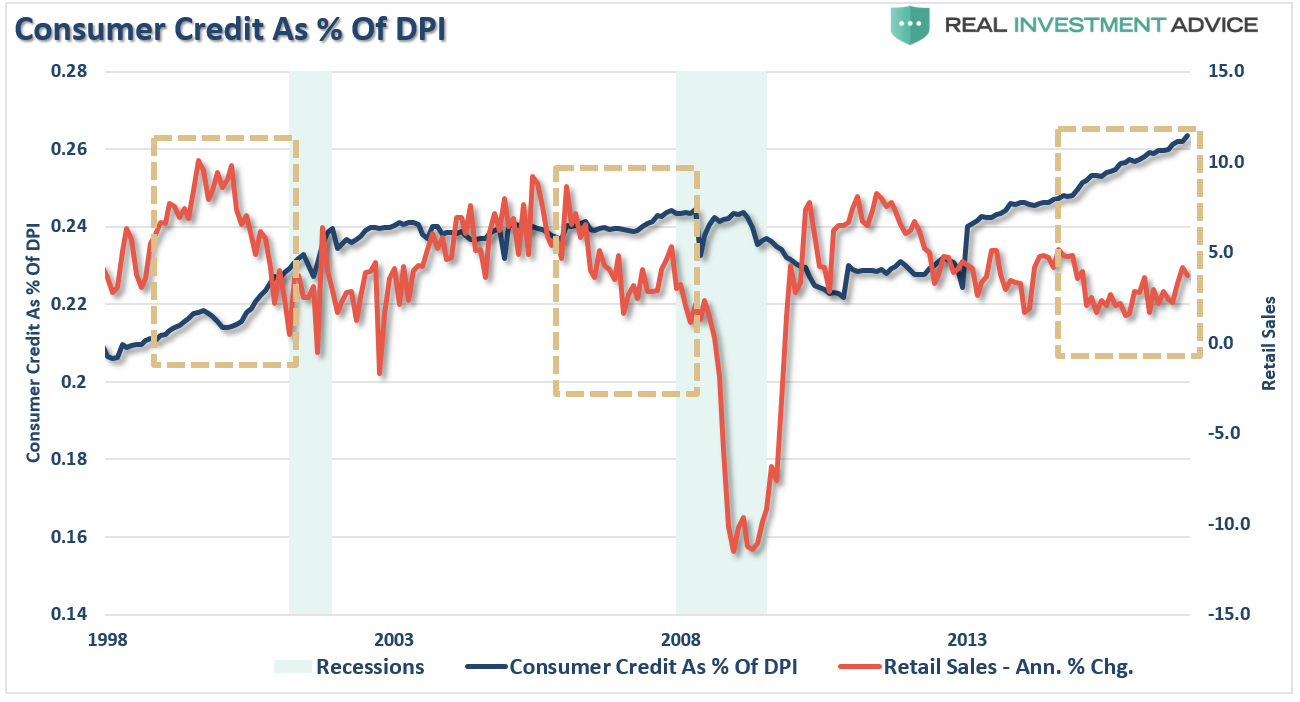

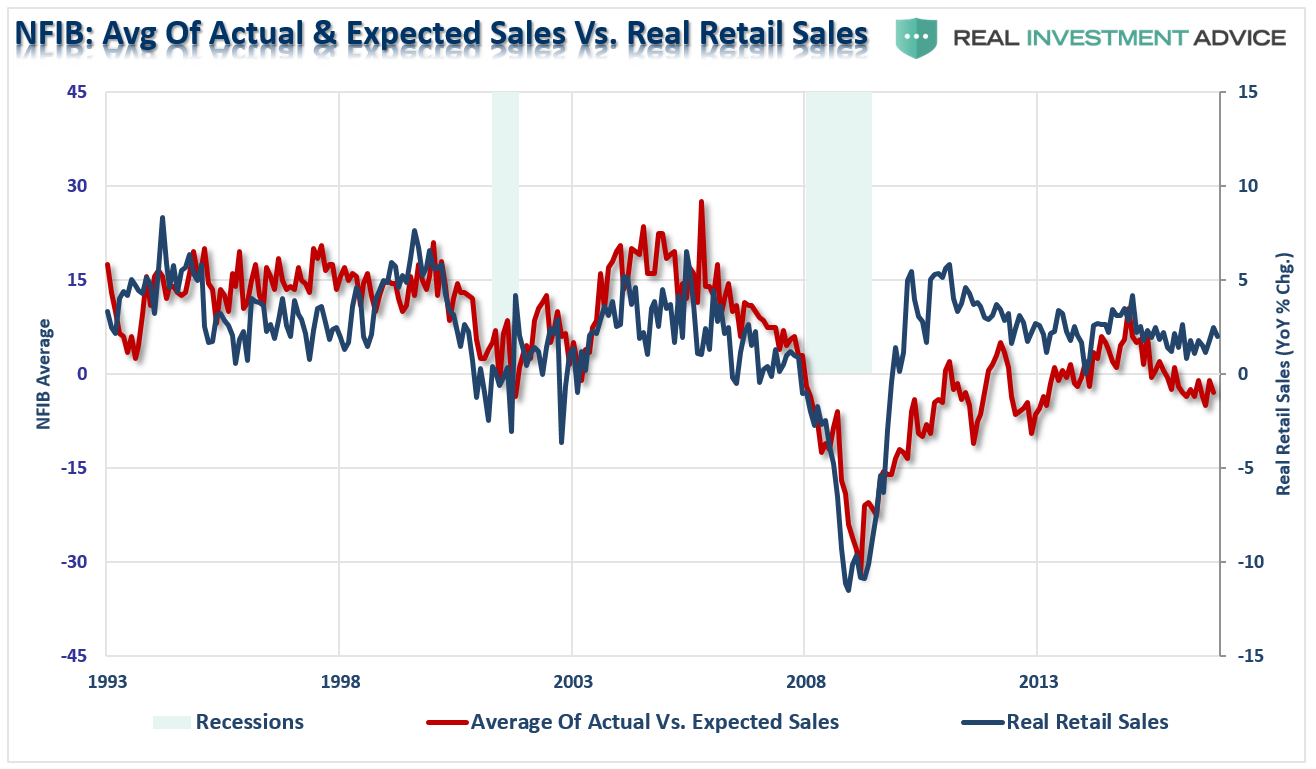

As more evidence of consumer’s struggling to maintain their standard of living, while consumer credit has continued to climb, retail sales remain weak as shown below.

And as the astute Greg S. pointed out yesterday:

YoY % change in $ amount of consumer delinquencies is disturbing.@LanceRoberts @RaoulGMI @ttmygh https://t.co/sl4aGY5lDS #FRED @stlouisfed

— Greg S., CFA (@GS_CapSF) January 11, 2017

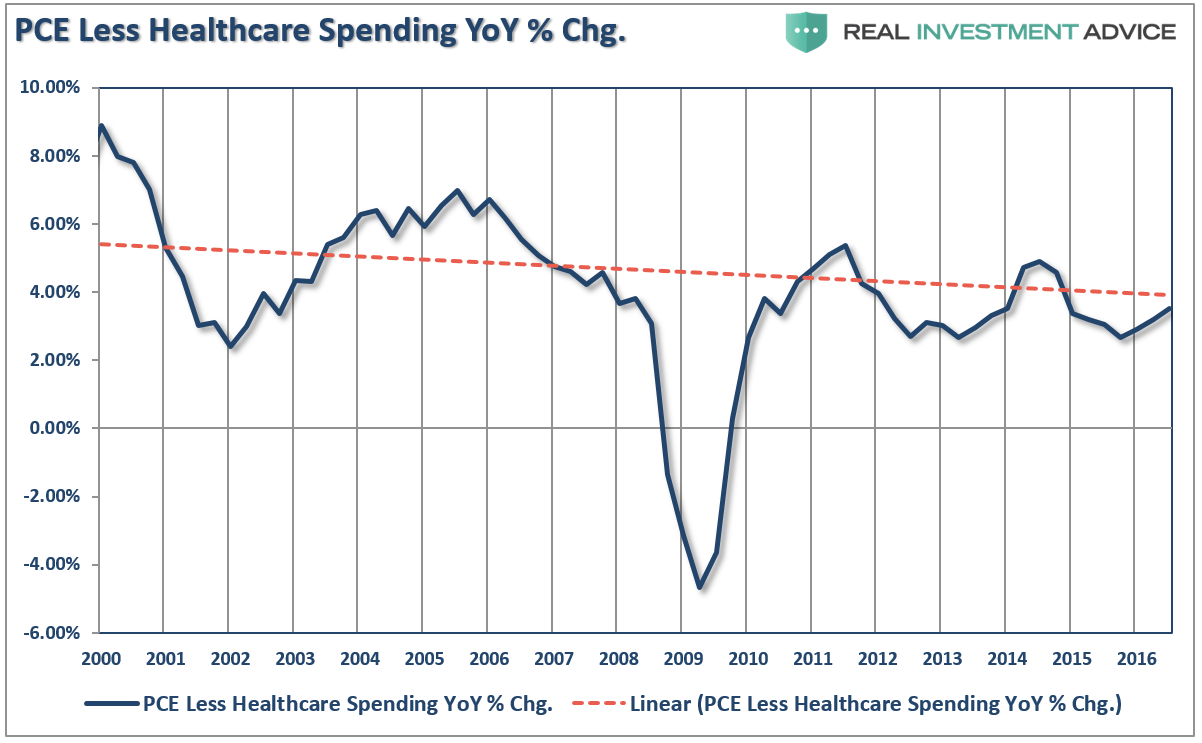

Rising credit and delinquency rates combined with stagnant wage growth and you have a wicked brew being mixed for the economy. Furthermore, once you strip out surging health care related costs the strength witnessed in economic and inflation related reports as of late seem much less optimistic. (This is an issue I have repeatedly warned of over the past several years.)

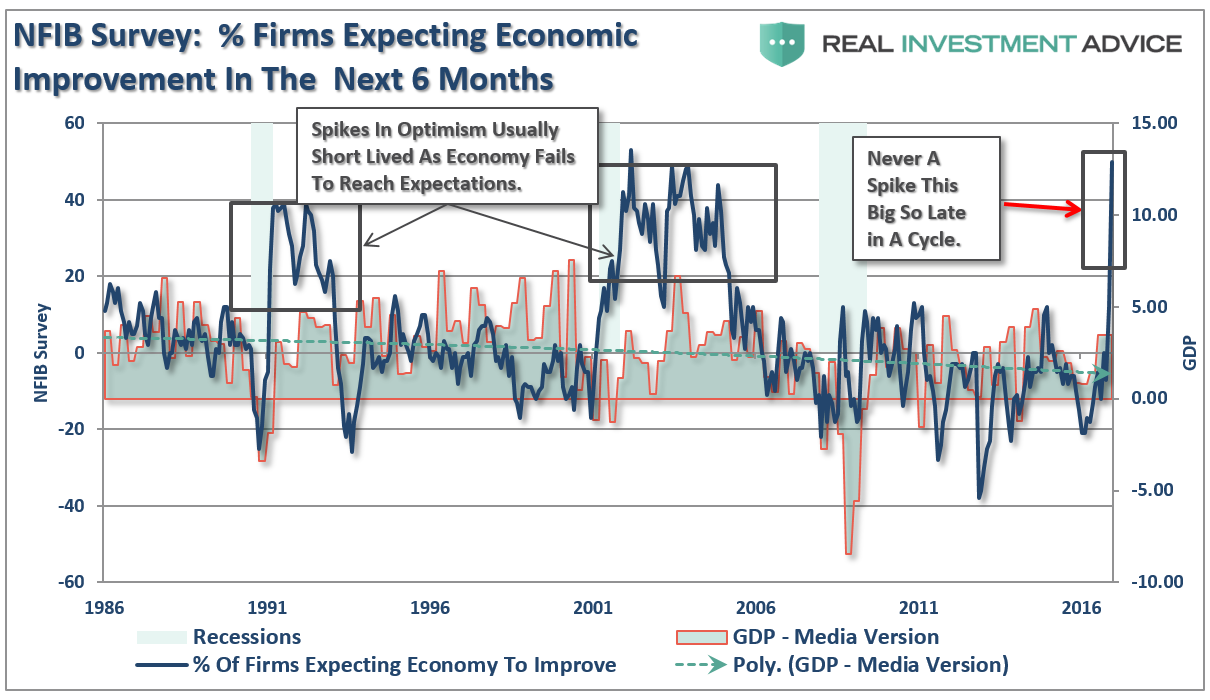

Despite surges in optimism, with roughly 70% of the economy dependent upon the consumer, the ability of consumers to continue leveraging consumption is limited. As wage growth continues to stagnate, except for the top 20% of those employed, economic growth will likely remain sluggish which suggests the recent surges in optimism, as I will discuss in a minute, will likely fade as “Trump-uberence” reconnects with “economic realities.”

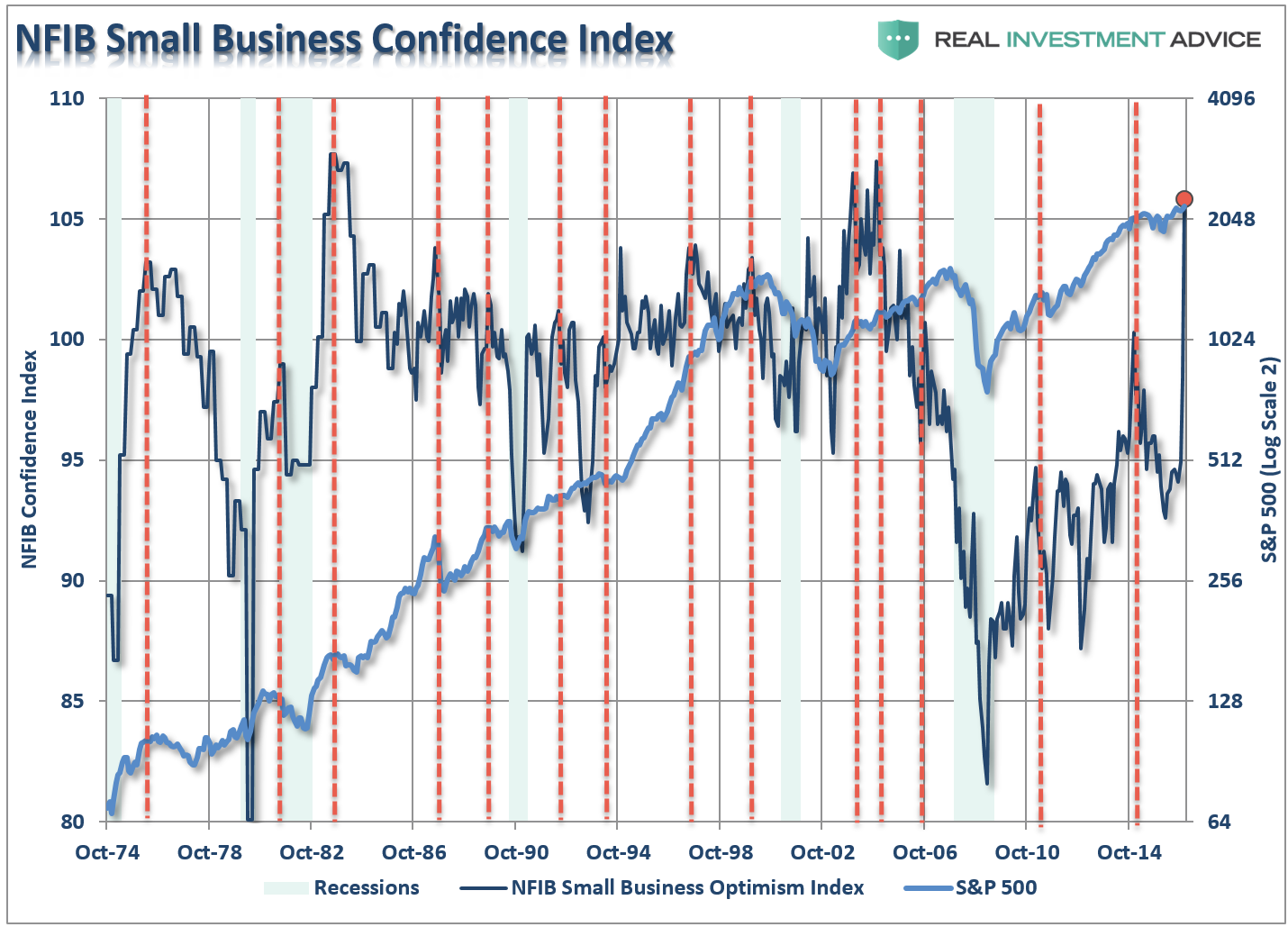

Besides the surge in consumer debt, optimism has also exploded since the Presidential election. In the latest NFIB Small Business Survey, respondent’s confidence surged to levels only seen twice before in history. Interestingly, this surge comes nearer the end of a long economic cycle versus a more expected post-recessionary rise seen previously. (In many cases, as noted by the vertical dashed lines, sharp spikes in confidence have coincided with short to intermediate-term market peaks.)

However, while the spike in confidence is certainly encouraging there are a couple of aspects about the survey that should be considered.

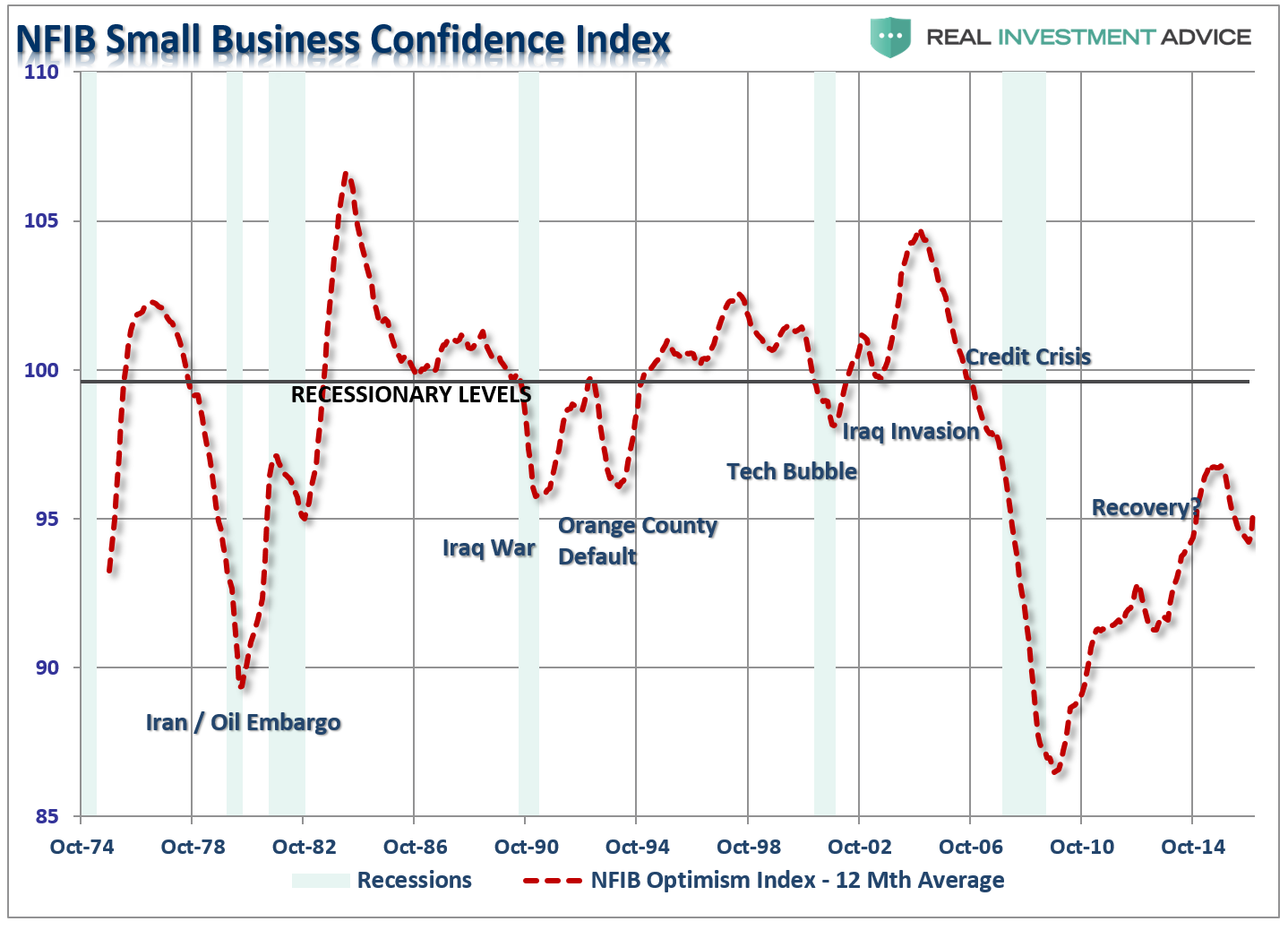

Furthermore, if we use a 12-month average of the survey to smooth out the volatility, a very different picture emerges and one that is likely far more consistent with the current state of the economy.

Importantly, “expectations” have tended to run well ahead of reality. As shown below while spikes in expectations have corresponded to short-term rises in economic activity, such increases have generally been very short-lived. This time around a much stronger dollar, rising interest rates, and plenty of potential policy missteps could quickly reverse “exuberance” back to “reality.”

Increases in confidence are one thing, but actually committing capital to projects, expenditures, equipment and further employment are based on actual increases in demand, not hope.

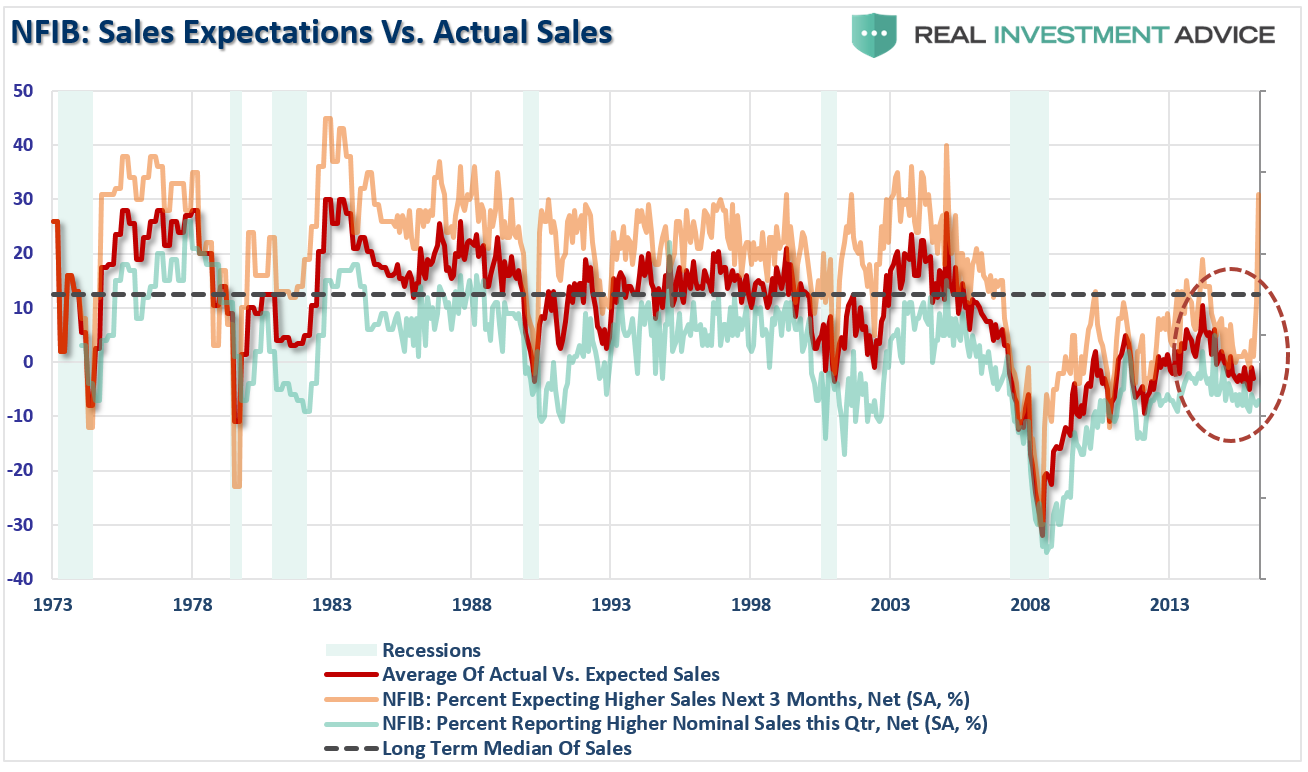

For evidence of demand, we can look at sales “expectations” versus actual “sales.” Not surprisingly, since the election, “expectations” of increased sales have surged. However, “actual sales” have been on the decline for several months due to the constriction of consumer demand due to increased debt and weak wage growth as noted above.

This also shows up in actual real, inflation adjusted, retail sales data which shows little momentum.

While the surge in “optimism” is certainly welcome, there is a function of an economic cycle that must be dealt with. As I discussed previously:

“It is not just tighter monetary policy weighing on fiscal policy changes but the economic challenges as well. As my partner Michael Lebowitz recently pointed out – ‘this ain’t the 1980’s.’

‘Many investors are suddenly comparing Trump’s economic policy proposals to those of Ronald Reagan. For those that deem that bullish, we remind you that the economic environment and potential growth of 1982 was vastly different than it is today.’

This also isn’t 2009 where economic activity and consumption is extremely depressed which gives tax cuts, incentives and regulatory reforms have a much bigger impact on economic and earnings growth.

Will “Trumponomics” change the course of the U.S. economy? I certainly hope so.

However, as investors, we must understand the difference between a “narrative-driven” advance and one driven by strengthening fundamentals. The first is short-term and leads to bad outcomes. The other isn’t, and doesn’t.”

While optimism and confidence has certainly surged over the last couple of months, something else has as well – policy uncertainty.

As I stated above, the surge in optimism from consumers, investors, and business owners has certainly lifted spirits, it hasn’t translated into fuel for economic growth as of yet. Interestingly, as Nick Timiraos from the WSJ notes, with free-trade adversaries on one side of his economic team and market-oriented advisers from the Washington and Wall Street establishments on the other, Donald Trump has charted an unpredictable course.

“A flat organizational structure could set these and other individuals against each other as they compete for Mr. Trump’s support. Uncertainty about his economic agenda is heightened by how Mr. Trump, who has never held public office, has changed his mind on some policy issues while saying little about others.

Tensions are already surfacing now that Mr. Trump must translate campaign promises into a governing agenda. Mr. Trump, and other Republican lawmakers, are voicing concerns over how quickly to advance a repeal of Mr. Obama’s health-care overhaul, which could boost deficits and leave millions without health insurance. The new administration also may ask for billions of dollars for border security after Mr. Trump repeatedly promised to make Mexico shoulder the cost of new security measures.

The nucleus of Mr. Trump’s economic team consists of two financiers, Mr. Cohn and Treasury secretary-designate Steven Mnuchin, who in 1994 both became partners at Goldman. They haven’t weighed in on the pitched partisan policy battles of the past decade, making them more of a tabula rasa who advisers say can translate into policy Mr. Trump’s fusion of traditional GOP support for lower taxes and fewer regulations with his calls to brand China as a currency manipulator and spend more on infrastructure.

The elevation of Goldman Sachs alums also stands in contrast to Mr. Trump’s pointed attacks on the investment bank in last fall’s campaign. In addition to Messrs. Cohn and Mnuchin, the transition team is considering Jim Donovan, a senior Goldman executive, to serve as undersecretary of domestic finance, a top Treasury Department post.

Perhaps the starkest example of policy idiosyncrasy comes with Mr. Trump’s pick for budget director, Rep. Mick Mulvaney (R., S.C.), a committed deficit hawk. He has been deeply critical of Republicans who have sought higher spending and spoke skeptically of Mr. Trump’s infrastructure-spending push just weeks after the November election.

Throughout the campaign, Mr. Trump championed more spending on everything from the military to infrastructure, veterans’ health care and border security while he also brushed aside calls to address to long-run solvency of popular benefit programs such as Medicare and Social Security.

One question now is whether Mr. Mulvaney will prevail on Mr. Trump to rein in his big-spending agenda, or whether he might be tasked by Mr. Trump to sell a short-term boost in federal outlays to his fellow, skeptical House conservatives.

The organizational structure ‘may leave everyone guessing about who holds ultimate sway,’ said Jeb Mason, a Treasury Department official in the George W. Bush administration.”

Importantly, with economic growth anemic, consumers stretched and an economy heading into one of the longest post-recessionary expansions on record, there is little room for a policy misstep at this juncture.

Maybe Trump will be wildly successful and the economy will come roaring back. That is a possibility.

But there is also the risk it won’t.

Optimism is one thing. Your personal capital and financial health is quite another.

Just some things I am thinking about.

via Motley Fool Headlines by on Thu, 12 Jan 2017 21:41:00 GMT

via by Tyler Durden on Thu, 12 Jan 2017 21:30:00 GMT

“I am grateful to the Department of Justice’s IG for taking on this review.

He is professional and independent and the FBI will cooperate fully with him and his office.

I hope very much he is able to share his conclusions and observations with the public because everyone will benefit from thoughtful evaluation and transparency regarding this matter.”

The day before, senior Justice Department leaders had warned Comey not to send the letter, because it violated two long-standing department policies — discussing an ongoing investigation and taking any overt action on an investigation so close to an election. At the time, it was less than two weeks before the election, and early voting had already begun.

Comey, too, has notably declined to talk about any possible investigations of President-elect Donald Trump or his campaign, as recently as this week rebuffing requests from legislators to confirm agents were looking into any such matters.

“I don’t—especially in a public forum, we never confirm or deny a pending investigation,” Comey said.

Comey sent a second letter to Congress on the Clinton case, just days before the election, declaring that the investigation was complete and he was not changing the decision he had made in July to recommend no charges. But the damage — in the minds of Clinton supporters, at least — had been done.

“Decisions that are made by inspectors general across the administration are independent," White House spokesman Josh Earnest told reporters. “Hopefully they will follow the evidence where it leads.

Finally, for those asking, Horowitz is an Obama appointee who has been a consistent Democratic donor over the years, including donations to Clinton's Senate bid, as well as longtime Clinton ally Richard Blumenthal (D-Conn.) and current Senate Minority Leader Chuck Schumer (D-N.Y.).

via by Tyler Durden on Thu, 12 Jan 2017 21:18:56 GMT

In a strange "hostile takeover" of state TV broadcasters, not to mention a bizarre moment of startling symmetry with the current state of American politics, C-SPAN, the public affairs network that broadcasts political proceedings the United States House of Representatives and Senate, was interrupted by a live feed of Russian TV channel, RT, formerly known as Russia Today.

The state-funded Russian news network, which was accused by the US intelligence community of spreading "fake news" and directly influencing the US elections, took over the online feed of C-SPAN1, which had been broadcasting a discussion in Congress regarding the Securities and Exchange Commission Regulatory Accountability Act, for about ten minutes at 2:30 pm ET.

As California Democrat Maxine Waters was speaking, the feed suddenly cut from the House floor to a broadcast of RT. The feed cut in with a commercial break before returning to the RT news desk, where an anchor spoke of a suicide bombing. As the IBT noted, multiple C-SPAN watchers (although hardly too many, as C-SPAN's Nielsen Ratings are even lower than those of CNBC) made mention of the sudden change on Twitter, including Deadspin editor Timothy Burke, who captured the moment the C-SPAN feed switched to RT.

Here's the moment Russia Today took over the C-SPAN1 feed. Unclear what happened. RT aired for about ten minutes before C-SPAN1 came back. pic.twitter.com/mhWVgCoFxF

— Timothy Burke (@bubbaprog) January 12, 2017

It is unclear what caused the issue, although some jokingly suggested, that this is yet another "hacking" of US media interests by Putin. Allaying concerns of a grassroots Russian takeover of US media by Russia, C-SPAN sent out a notice later stating that the mix up was due to an "internal routing issue."

"an internal routing issue" pic.twitter.com/1Htue3Ef61

— Alex Kantrowitz (@Kantrowitz) January 12, 2017

via Motley Fool Headlines by on Thu, 12 Jan 2017 21:15:00 GMT

via by ZeroPointNow on Thu, 12 Jan 2017 21:09:01 GMT

With eyebrows suspiciously furrowed, Tucker Carlson sat down tonight with NYU Professor of Russian Studies and contributor to The Nation, Stephen Cohen, to discuss the 35 page #FakeNews dossier which has gripped the nation with nightmares of golden showers and other perverted conduct which was to be used by Russia to keep Trump on a leash.

With eyebrows suspiciously furrowed, Tucker Carlson sat down tonight with NYU Professor of Russian Studies and contributor to The Nation, Stephen Cohen, to discuss the 35 page #FakeNews dossier which has gripped the nation with nightmares of golden showers and other perverted conduct which was to be used by Russia to keep Trump on a leash.

The left leaning Cohen, who holds a Ph.D. in government and Russian studies from Columbia, taught at Princeton for 30 years before moving to NYU. He has spent a lifetime deeply immersed in US-Russian relations, having been both a long standing friend of Mikhail Gorbachev and an advisor to President George H.W. Bush. His wife is also the editor of uber liberal "The Nation," so it's safe to assume he's not shilling for Trump - and Tucker was right to go in with eyebrows guarded against such a heavyweight, to say the least.

Cohen, who has been quite vocal against the Russophobic witch hunt gripping the nation, believes that this falsified 35 page report is part of an "endgame" to mortally wound Trump before he even sets foot in the White House, by grasping at straws to paint him as a puppet of the Kremlin. The purpose of these overt attempts to cripple Trump, which have relied on ham-handed intelligence reports that, according to Cohen "even the New York Times referred to as lacking any evidence whatsoever," is to stop any kind of détente or cooperation with Russia.

Cohen believes that these dangerous accusations attempting to brand a US President as a puppet of a foreign government constitute a "grave American national security threat."

At the very end of the interview, Tucker's very un-furrowed eyebrows agreed.

See below:

via Motley Fool Headlines by on Thu, 12 Jan 2017 21:05:00 GMT

via by Tyler Durden on Thu, 12 Jan 2017 21:02:20 GMT

For Nasdaq traders today...

Small Caps (and briefly The Dow) sunk into the red for 2017... (NOTE: the moment Trannies and The Dow tagged unchanged for 2017 a miracle bid appeared)...

Second day in a row if VIX-smashing, panic-V-shaped-recovery-stock-buying...

Though we note it seems all about the European close once again...

They were desperate to get Nasdaq green into the close...

In fact everything jumped after Europe closed...

Nasdaq broke it's winning streak...

While everything bounced, financials were the day's laggards while Utes and Healthcare managed to get green by the close...

Treasury yields rose and steepened notably after the 30Y auction...(same as yesterday) but remain lower on the week...

Not helped by clear pressure for steeper curves from The Fed...

The USD Index plunged to its 50-day-moving-average...almost erasing all the post-FOMC gains...

And bounced...

The USD bounce back was led by GBP and JPY weakness...

Gold is having a great week while crude remains red...

But as the dollar, bond yields, and stocks ramped hard in the afternoon, gold limped back below $1200...

via by Tyler Durden on Thu, 12 Jan 2017 20:55:00 GMT

Following central bank governor Agustin Castens' comments earlier in the day that "intervention is a tool to smooth changes in currency value," and "Trump’s win has created uncertainty on Mexico’s growth model," Mexican Peso traders have come up with unusual solution: instead of dumping billions in intervention with no effect, buy Twitter and shut it down.

As Bloomberg reports, the strange idea has a certain logic to it...

It goes like this: Instead of spending its precious reserves to defend the peso, Mexico should just buy Twitter Inc. -- at a cost of about $12 billion -- and immediately shut it down.

The notion made the rounds this week after the central bank revealed it had already blown through $2 billion of reserves in a largely futile effort to shield the peso from a steady stream of anti-Mexico Tweets from Donald Trump.

“I would suggest they do it fast,” joked Juan Carlos Alderete, a foreign-exchange strategist at Banorte-Ixe in Mexico City. “Because we can barely afford it now."

Of course this is unlikely to happen, but, quite frankly, it has more chance of success than the vicious circle Mexico is about to find itself in.

via by Tyler Durden on Thu, 12 Jan 2017 20:45:59 GMT

While the Fed watchers have been obsessing in recent weeks about the pace and size of any upcoming Fed rate hikes, summarized best by Dallas Fed president Robert Kaplan who earlier today said:

... and unexpected new buzzword emerged today, namely Fed balance sheet unwind when first Philly Fed's Steve Harker noted it in his speech earlier this morning...

followed later in the day by St. Louis Fed's James Bullard who, likewise, hinted that selling Fed assets may be coming soon:

Of course, how credible it is that the the Fed may actually engage in this is anyone's guess: should the Fed "unexpectedly" start to reduce its balance sheet, the impact on global yields would be devastating, and make the Taper Tantrum and the TanTrump seems like child's play in comparison. Which, perhaps, is why today for the first time we got not one but two such "trial balloons" from two separate Fed presidents, just to gradually acclimate the market with the concept of upcoming balance sheet normalization.

The mechanics of such a process are rather mindboggling, especially coming at a time when even the Republicans are pushing to layer on an addition $9 trillion in US government debt over the next decade, which - all else equal - would mean require more QE to monetize the deficit, precisely the opposite of selling Fed-owned Treasuries.

Then again, the Fed has been known to make major, and quite public, mistakes. Whether this is one of them, and whether it is intentional remains to be seen, however the sharp steepening in the curve that has taken place today amid the sudden Fed talk of Fed balance sheet unwinding, is very much unmistakable.

The only (perhaps rhetorical) question is how such an unwind won't impact stocks far more than bonds. And then we remember that nothing can possibly ever have an adverse impact on stocks, and all is again well with the world.

via Motley Fool Headlines by on Thu, 12 Jan 2017 20:31:00 GMT

via by Tyler Durden on Thu, 12 Jan 2017 20:27:42 GMT

The last time TCW's Ted Rivelle, whose firm at last checked managed roughly $195 billion, issued a warning was back in late September, when he cautioned that the "central banking Emperors have no clothes... when the supposed solutions to the Fed’s dilemma are merely new “problems,” you know you are approaching the cycle’s end... successful, long-term investing is predicated on not just knowing where the happening parties are during the reflationary parts of the cycle but, even more importantly, knowing when the time has come to leave the dance floor. In our view, that time has already come."

He was both right and wrong: right in that the central banking emperors indeed are naked, and the era of monetary stimulus is ending; wrong in that the time to leave the dance floor had certainly not yet arrived.

What Rivelle didn't anticipate is that a new "emperor" (one with clothes for now), emerged, and has vowed to pick up the baton of monetary policy, using it to create trillions in fiscal stimulus instead.

His name was Donald Trump, and at least until now, the markets have been transfixed by his ability to promise broad generalities while delivering nothing in terms of actionable plans. Of course, he is not even a president yet, so one can't fault Trump, yet, and it is understandable why the honeymoon period has lasted as long as it has, but sooner or later, Trump will have to give the market something more.

And since there is a rapidly rising risk that he won't, both Morgan Stanley and Jeff Gundlach have recently told traders to "sell the inauguration."

They are not alone, because as TCW's Ted Rivelle writes in his latest letter "No Stagnation Without Representation", while there will be long-term consequences of Trump's policies, assuming they are implemented as expected, the costs will arrive long before the expected benefits - after all they are already being discounted by various assets classes such as rates and the dollar - and eventually have a spillover effect on equities. Among these are: i) higher Treasury rates, ii) stronger dollar, iii) the China economy and iv) undercapitalized continental European banks.

Rivelle's bottom line: nothing has actually changed.

"in our estimation the investment climate for risk assets after the election looks a lot like the environment before the election: risky. And while there are many valid reasons to cheer a change in tax policy, saving the U.S. and global economy from its past excesses is not one of them. Stay cautious, my friend."

His full note is below.

No Stagnation Without Representation, By Tad Rivelle

Over the course of this asset price cycle, central banks have held the rate markets in thrall. Until now. Low for longer just slammed head-on into November’s altered political realities. While the detailed content of Trumponomics has yet to be revealed, the broad outlines are apparent: comprehensive tax cuts, regulatory roll-back, and, more speculatively, an infrastructure program. The rate market’s “first draft” reaction to a Fed that has had its low rate car keys taken away and a Federal government about to massively balloon its borrowing requirements has been predictable: higher Treasury rates.

TOTAL FEDERAL DEFICITS/SURPLUS, As a percentage of GDP

Sources: Congressional Budget Office, Tax Policy Center, Cornerstone Macro

Global Yields Rise After the Election

Source: Bloomberg

Higher rates have, in turn, made dollar assets look more attractive, promoting a sharp rise in the dollar’s exchange value:

U.S. Dollar Appreciation Since The Election Night

Source: Bloomberg

So, are markets telling us that with the new year we augur in a new era of prosperity? Or, does the financial baggage carried along from the past six or seven Christmases mean that investors must still navigate an aging credit cycle, fraught with all manner of latecycle risks? Put differently, is it really feasible for fiscal policy to restart the cycle “anew” given years and years of financial excess?

Well before tipping our hand, let’s acknowledge that cutting taxes and whittling down the regulatory state should lift productivity and enhance growth – over the long term. “Long-term” in this case likely means well after this current cycle has sung its swan song. But, there will be near-term benefits. If we think of the domestic economy as having three parts, ie. government, business, and the consumer, then, almost tautologically, the operating “deficits” of one become the combined “surpluses” of the others (see figure on following page). If government goes further into deficit, consumers and businesses see the benefit in the form of higher incomes and profitability. But, these are the most immediate and visible effects of the changing policy regime.

Yet, the lowering of the Federal take from the economy is hardly costless and will have lagged consequences. Furthermore, the lagged consequences of today’s pending policy changes have already been at least partially discounted by forward looking markets into higher Treasury rates and a stronger dollar. And, even lagged consequences will, in turn, have their own lagged consequences. Consider:

1. Higher Treasury rates. Interest rates powerfully impact asset prices and the general economy. Notably: (1) rising capitalization rates pressure asset prices; (2) the already overgeared U.S. investment grade sector may find itself hard pressed to “maintain rating” as borrowing costs elevate; (3) higher home mortgage rates further stretch home affordability, potentially derailing one of the brighter spots in the U.S. economy; (4) a wider rate differential between the U.S. and Europe and between the U.S. and Japan may exacerbate an on-going flight of capital from overseas, placing upward pressure on euro and yen denominated rates.

2. Stronger dollar. The dollar holds a unique position in the global economy, and a rapidly rising dollar exchange rate has historically caused something, somewhere in the global economy to “break.” Those in the EM that have borrowed in dollars face the reality of a liability stream that has become more expensive to repay. Meanwhile, the second largest economy on the planet, China, has informally pegged the yuan to the dollar. A stronger dollar generally means a stronger yuan; a stronger yuan means a less competitive export sector for an economy whose “mother’s milk” is trade.

3. China economy. Many believe the China economy to be well managed and with $3 Trillion in FX reserves, who really wants to argue the point? Yet, large nations have a way of “exporting” their troubles, in the manner that was attributed (in the 1960s) to then U.S. Treasury Secretary John Connally when he quipped that the “dollar was our currency, but your problem.” Suppose China finds that its domestic growth continues to slow. What are its choices? China can “unpeg” the yuan and allow it to depreciate, so as to maintain Chinese export competitiveness. That’s good news for China, but might be a disaster for weaker links in the EM that are unable to adjust to a lower yuan. Or, China might sell-off some of its stockpile of Treasuries so as to finance domestic consumption at a time when its exports are weak. The likely ceteris paribus result would be higher dollar interest rates and, you guessed it, a still stronger dollar. Yep, the yuan is their currency, but it could be your problem.

CHINA’S SUPPORT OF THE RMB REFLECTED IN DECLINING FX RESERVE BALANCE

Source: Bloomberg

4. Undercapitalized continental European banks. Unlike the U.S., Europe barely recapitalized its banks after the 2008 crisis. Worse, with a negative rate environment and a slow growing economy, the European banks are accreting new capital at a snail’s pace. Some say that so long as the national governments have the back of the European money center banks that perhaps low capital ratios are irrelevant. Yet, let’s not forget that those who are not credit-worthy, don’t get credit. Inadequate capital levels raise the specter that European banks remain vulnerable to a “liquidity” crisis when times get tough. And, bereft of U.S. depository gathering facilities, the only way a European bank can get its hands on U.S. dollars is wholesale, likely via the capital markets. The ECB may be a European bank’s best friend in a crisis but that might be thin consolation if the bank is shut-out of the capital markets and in desperate need of dollars. And with problem loans running at an EU average of 20%, you don’t even have to be a bond guy to foresee trouble ahead.

U.S. vs. European Tangible Common Equity Ratios (%)

Source: SNL Financial

Total problem loan ratio, by country

Source: Deutsche Bank; *Includes Greece and Cyprus (not shown) with totals above 50%.

So, in our estimation the investment climate for risk assets after the election looks a lot like the environment before the election: risky. And while there are many valid reasons to cheer a change in tax policy, saving the U.S. and global economy from its past excesses is not one of them. Stay cautious, my friend.

via Motley Fool Headlines by on Thu, 12 Jan 2017 20:22:00 GMT