Feed Aggregator Page 623

Rendered on Tue, 17 Jan 2017 23:30:08 GMT

Rendered on Tue, 17 Jan 2017 23:30:08 GMT

via Motley Fool Headlines by on Tue, 17 Jan 2017 22:45:00 GMT

via Motley Fool Headlines by on Tue, 17 Jan 2017 22:41:00 GMT

via by Tyler Durden on Tue, 17 Jan 2017 22:15:00 GMT

Submitted by Jonathan Rochford via Narrow Road Capital,

The recent blow-up of the Dallas Police and Fire Pension System was entirely predictable. Whilst it is tempting to blame unusual circumstances for the recent lock-up of redemptions and likely substantial reductions to pensions for those still in the fund, many other American pension funds are heading down the same road. The combination of overpriced financial markets, inadequate contributions and overly generous pension promises mean dozens of US local and state government pension plans will end up in the same situation. The simple maths and political factors at play mean what happened at GM, Chrysler, Detroit and now Dallas will happen nationwide in the coming decade. So, what’s happened in Dallas and why will it happen elsewhere?

Background to the Dallas Pension Fiasco

The Dallas pension scheme has been underfunded for many years with the situation accelerating recently. As the table below shows, as at 1 January 2016 the pension plan had $2.68 billion of assets (AVA) against $5.95 billion of liabilities (AAL), making the funding ratio (AVA/AAL) a mere 45.1%. Despite equity markets recovering strongly over the last seven years, the value of the assets has fallen at the same time as the value of the liabilities has grown rapidly. The story of how such a seemingly odd outcome could occur dates back to decisions made long before the financial crisis.

Source: Dallas Police and Fire Pension System

In the late 1990’s, returns in financial markets had been strong for years leading many to believe that exceptional returns would continue. In this environment, the board that ran the Dallas plan decided that more generous pension terms could be offered to employees and that these could be funded by the higher expected returns without needing greater contributions from the Dallas municipality and its taxpayers. Exceptionally generous terms were introduced including the now notorious DROP accounts and inflated assumptions for cost of living adjustments (COLA). These changes meant that pension liabilities were guaranteed to skyrocket in future years, whilst there was no guarantee that investment returns and inflation levels would also be high. Dallas police and fire personnel were being offered the equivalent of a free lunch and they took full advantage.

In the 2000’s the pension plan made some unusual investment decisions. A disproportionate amount of plan assets were invested in illiquid and exotic alternative investments. When the financial crisis struck these assets didn’t decline as much as the assets of other pension plans. However, this was merely a deferral of the inevitable write downs which came in the last two years after a change in management.

Recent Events

Throughout 2016 the pension board, the municipality and the State government bickered over who was responsible and who should pay to fix the mess. The State government blamed the municipality for the poor investment decisions. The municipality blamed the State government for creating a system that it could not control but was supposed to be responsible for. It also blamed the pension board for the overly generous changes they implemented. The pension board recognised the huge problem but offered only minor concessions arguing that plan participants were entitled to be paid in full in all circumstances. They asked the municipality for a one-off addition of $1.1 billion, equivalent to almost one year’s general fund revenue for the municipality.

As the funding ratio plummeted during 2016, plan participants became concerned that their generous pension entitlements might not be met. In other pension plans the employer might increase its contributions when these circumstances occurred, but in Dallas the municipality was already paying close to the legislative maximum. Police officers with high balances retired in record numbers, pulling out $500 million in four months in late 2016. Those who withdrew received 100% of what was owed, with those remaining seeing their position as measured by the funding ratio deteriorate further.

In November, when faced with $154 million of redemption requests and dwindling liquid assets, the pension board suspended redemptions. The funding ratio is now estimated to be around 36% with assets forecast to be exhausted in a decade. Litigation has begun with some plan participants suing to see their redemption requests honoured. The municipality has indicated it wants to claw back some of the generous benefits accrued since the changes in the 1990’s, though this is likely to only impact those who didn’t redeemed. The State has begun a criminal investigation. Everyone is looking to blame someone else, but not everyone has accepted that drastic pension cuts are inevitable.

The Interplay of Political Decisions and Financial Reality

The factors that led to Dallas pension fiasco are all too common. Politicians and their administrations often make decisions that are politically beneficial without taking into account financial reality. A generous pension scheme keeps workers and their unions onside, helping the politicians win re-election. However, the bill for the generosity is deferred beyond the current political generation, with unrealistic assumptions of future returns enabling the problem to be obscured. As financial markets tend to go up the escalator and down the elevator it is not until a market crash that the unrealistic return assumptions are exposed and the funding ratio collapses.

This is when a second political reality kicks in. In the case of Dallas, there are just under 10,000 participants in the pension plan compared to 1.258 million residents in the municipality. Plan participants therefore make up less than 1% of the population. If the Dallas municipality chose to fully fund the pension plan it would be require an enormous increase in taxes from the entire population in order to fund overly generous pensions for a very small minority of the population. For current politicians, it is far easier to blame the previous politicians and the pension board for the mess and see pensions for a select group cut by half or more than it is to sell a massive tax increase.

The legal position remains murky and it will take some time to clear up. The municipality is paying 37.5% of employee benefits into the pension plan, the maximum amount required by state law. Without a change in state legislation, it seems likely that the pension plan will have to bear almost all of the financial pain through pension reductions. If state legislation was changed to increase the burden on the municipality years of litigation could ensue with the potential for the municipality to declare bankruptcy as a strategic response. The appointment of an administrator during bankruptcy could see services reduced and/or taxes increased, but pension cuts would be all but a certainty.

Dallas Isn’t the First and Won’t be the Last

It’s tempting to see the generous pension structure and bad investment decisions in Dallas as making it a special case. Detroit was seen by many as a special case when it went into bankruptcy in 2013 as it had seen its population fall by 25% in a decade. This depopulation left a smaller population base trying to fund the debt and pensions obligations incurred when the population was much larger. Growing debt and pension obligations are signs of what is to come for many local and state governments who have been living beyond their means for decades.

As well as building up pension obligations many US governments have been accruing explicit debt. The two are intertwined, with some governments issuing debt to make payments into their pension plans, often to close the underfunding gap. This is very much a short-term measure, as whether it is pension contributions or debt repayments both will either require high taxes and/or lower spending on government services in the future in order for these payments to be met.

Pew Charitable Trusts research estimates a $1.5 trillion pension funding gap for the states alone, with Kentucky, New Jersey, Illinois, Pennsylvania and California going backwards at a rapid rate. Using a wider range of fiscal health measures the Mercatus Center has the five worst states as Kentucky, Illinois, New Jersey, Massachusetts and Connecticut. The table below shows the five state pension plans in Illinois, with an average funded ratio of just 37.6%.

Source: Illinois Commission on Government Forecasting and Accountability

For cities, Chicago is likely to be the next Detroit with the city and its school system both showing signs of financial distress. Chicago is trying to stem the bleeding with a grab bag of tax and other revenue increases but in the long term this makes the overall position worse.

Default is Almost Inevitable as the Weak get Weaker

The problem for Chicago and others trying to pay their debt and pension obligations by raising taxes is that this makes them unattractive destinations for businesses and workers. Growth covers many sins, as growth creates more jobs and drags more people into the area. This increases the tax base and lessens the burden from previous commitments on those already there. Well managed, low tax jurisdictions benefit from a positive feedback loop.

For states and municipalities in decline, their best taxpayers are the first to leave when the tax burden increases. Young college educated workers with professional jobs generate substantial income and sales tax revenue but require little in the way of education and healthcare expenditure. This cohort has many options for work elsewhere and can easily relocate. Chicago and Illinois are bleeding people, with the flight of millionaires particularly detrimental on revenues.

Those who own property are caught in a catch 22; property taxes and declining population have pushed property prices down, potentially creating negative equity. But staying means a bigger drain on the household budget as property taxes are the most efficient way to raise revenue and therefore become the tax increased the most. If too many people leave property prices plummet as they have in Detroit, making it even more difficult to collect property taxes as these are typically calculated as a percentage of the property valuation. Bankruptcy becomes inevitable as a poorer and older population base that remains simply cannot support the debt and pension obligations incurred when the population base was larger and wealthier.

Pensions Will be Reduced, but Bondholders Will Fare Worst

The playbook from the Detroit bankruptcy is likely to be used repeatedly in the coming decade. When a bankruptcy occurs and an administrator is appointed a very clear order of priority emerges.

The Next Crisis Will Trigger an Avalanche

At the risk of being labelled a Meredith Whitney style boy who cried wolf I expect that the next financial crisis will trigger a wholesale revaluation of the creditworthiness of US state and local government debt. I have no crystal ball for when this will happen, but it is almost certain that the next decade will contain another substantial decline in asset prices. This will impact state and local governments and their pension obligations in two major ways.

Conclusion

Chronic budget deficits, growing indebtedness, excessive pension return assumptions and pension underfunding all set the stage for a wave of state and local government pension and debt defaults in the coming decade. As Detroit has shown this century, once an area loses its competitiveness its financial viability spirals downward. As taxes increase and services are cut the wealthiest and highest income earners leave slashing government revenues and increasing the burden on the older and poorer population that remains.

The next substantial fall in asset prices will sharpen the focus on budget deficits and pension underfunding, with the most indebted and underfunded states likely to find they are unable to rollover their debts at any price. Remaining residents will be negatively impacted, pensioners will see their payments slashed and bondholders will recover little, if any, of their debt. As there is virtually no political will to take action to avoid these problems investors should position their portfolios in expectation that these events will happen.

via Motley Fool Headlines by on Tue, 17 Jan 2017 22:27:00 GMT

via Motley Fool Headlines by on Tue, 17 Jan 2017 22:26:00 GMT

via Motley Fool Headlines by on Tue, 17 Jan 2017 22:23:00 GMT

via Motley Fool Headlines by on Tue, 17 Jan 2017 22:13:00 GMT

via Motley Fool Headlines by on Tue, 17 Jan 2017 22:09:00 GMT

via Motley Fool Headlines by on Tue, 17 Jan 2017 22:03:00 GMT

via by Tyler Durden on Tue, 17 Jan 2017 21:59:00 GMT

As we observed in yesterday morning's market wrap, while US market were taking the day off for the MLK holiday, China was busy defending an accelerating selloff across its stock markets.

During Monday trading, having traded quietly lower for the past few days, Chinese stocks tumbled in early trading on the mainland and in Hong Kong’s offshore market amid weakness in Asian equities. The Shanghai Composite Index dropped as much as 2.2% to head for its fifth loss in as many days, its longest losing streak since Aug. 2015.However a sudden bout of late afternoon buying sent the loss down to just -0.3%, on speculation China's national team was once again back in the markets.

The exact same pattern emerged overnight as well:

Very much like the previous day, China's CSI 300 Index climbed 0.2% on Tuesday, after earlier losing as much as 0.8%. On Monday, the index recovered from an intraday drop of 1.7% to close little changed, with some traders speculating the afternoon rally was caused by state buying.

We now have confirmation that, indeed, after a long hiatus, it was precisely the "national team" that had made an appearance, and was propping up stocks with an explicit directive: don't let stocks drop during Xi Jinping's trip to Davos. It is almost as if it is a rite of passage for Davos participants to demonstrate how effective they are at manipulating their stock market.

As Bloomberg reports today, China has taken "steps" to support its stock market this week - by which it means ordered various central bank conduits to buy stocks during selloffs - "according to people familiar with the matter, as President Xi Jinping’s appearance at the World Economic Forum in Davos puts Asia’s largest economy in the global spotlight."

Apparently China did not question what it would look like once it emerged that it is manipulating its market to give the false impression of stability at a time when Xi was addressing Davos, and expounding on the glorious benefits of globalization and liberalization... if not so much for asset price discovery or the yuan, of course.

State-owned investors bought shares to steady the market on Monday, while some funds were guided on Tuesday not to sell holdings with big weightings in benchmark indexes, the people said, asking not to be identified because they aren’t authorized to discuss the matter publicly. China’s securities regulators asked funds and brokerages to trade prudently this week and directed exchanges to report any abnormal transactions, the people said.

To be sure, Chinese authorities have traditionally intervened in markets before and during events of political significance, with government funds stepping in to boost stocks before a key meeting of the National People’s Congress last year and before a 2015 military parade celebrating the 70th anniversary of the World War II victory over Japan.

"China is doing this probably because it wants to paint an image of positivity as President Xi attends Davos," said Tommy Xie, an economist at Oversea-Chinese Banking Corp. in Singapore. Stocks will continue to be volatile as the nation’s monetary conditions tighten, Xie said.

Earlier today, taking the role of the world's globalist savior and free trade savior, and the "free world's" foil to the protectionist Trump, Xi - in the first visit by a Chinese leader to the World Economic Forum - told a Davos audience that “protectionism is like locking yourself in a dark room, which would seem to escape wind and rain, but also block out the sunshine. No one is a winner in a trade war.”

His audience was delighted to lap it up, despite the glaring contradictions of China's firewall, pervasive government subsidies of exporters, and constant WTO regime violations. Oh, and zero freedom of speech or human rights, of course.

Which may explain why China is engaging in outright market manipulation merely to show how "strong" its market (and thus economy) is. After all, such interventions are nothing more than a sleight of hand and an indication of how little the Communist Party thinks of the intelligence of its counterparties: surely one has to be very obtuse to be fooled by such a glaring intervention that "all is well." Yet the message sent by Xi to the world's "smartest and most powerful" people is that according to the Chinese president, they are on the same intellectual level as a few dozen million daytrading housewives.

We are confident all of this will be lost on the "Davos elite."

via by Tyler Durden on Tue, 17 Jan 2017 21:25:21 GMT

Following urges by Edward Snowden and Julian Assange (who offered his own extradition), President Obama has largely commuted the remaining prison sentence of Chelsea Manning, the army intelligence analyst convicted of an enormous 2010 leak that revealed American military and diplomatic activities across the world, disrupted the administration, and made WikiLeaks, the recipient of those disclosures, famous.

As The New York Times reports, the decision by Mr. Obama rescued Ms. Manning, who twice tried to commit suicide last year, from an uncertain future as a transgender woman incarcerated at the male military prison at Fort Leavenworth, Kan.

She has been jailed for nearly seven years, and her 35-year sentence was by far the longest punishment ever imposed in the United States for a leak conviction.

Now, under the terms of Mr. Obama’s commutation announced by the White House on Tuesday, Ms. Manning is set to be freed in five months, on May 17 of this year, rather than in 2045.

The commutation also relieved the Department of Defense of the difficult responsibility of her incarceration as she pushes for treatment for her gender dysphoria — including sex reassignment surgery — that the military has no experience providing.

As The New York Times describes, Ms. Manning was still known as Bradley Manning when she deployed with her unit to Iraq in late 2009. There, she worked as a low-level intelligence analyst helping her unit assess insurgent activity in the area it was patrolling, a role that gave her access to a classified computer network.

She copied hundreds of thousands of military incident logs from the Afghanistan and Iraq wars, which, among other things, exposed abuses of detainees by Iraqi military officers working with American forces and showed that civilian deaths in the Iraq war were likely much higher than official estimates.

The files she copied also included about 250,000 diplomatic cables from American embassies around the world showing sensitive deals and conversations, dossiers detailing intelligence assessments of Guantánamo detainees held without trial, and a video of an American helicopter attack in Baghdad in two Reuters journalists were killed, among others.

She decided to make all these files public, as she wrote at the time, in the hope that they would incite “worldwide discussion, debates, and reforms.” WikiLeaks’ disclosed them — working with traditional news organizations including The New York Times — bringing notoriety to the group and its founder, Julian Assange.

The disclosures set off a frantic scramble as Obama administration officials sought to minimize any potential harm, including getting to safety some foreigners in dangerous countries who were identified as having helped American troops or diplomats. Prosecutors, however, presented no evidence that anyone was killed because of the leaks.

In her commutation application, Ms. Manning said she had not imagined that she would be sentenced to the “extreme” term of 35 years, a term for which there was “no historical precedent.” (There have only been a handful of leak cases, and most sentence are in the range of one to three years.)

“I take full and complete responsibility for my decision to disclose these materials to the public,” she wrote.

“I have never made any excuses for what I did. I pleaded guilty without the protection of a plea agreement because I believed the military justice system would understand my motivation for the disclosure and sentence me fairly. I was wrong.”

The US Constitution allows a president to pardon "offenses against the United States" and commute -- either shorten or end -- federal sentences. Obama has so far granted 148 pardons since taking office in 2009 -- fewer than his predecessors, who also served two terms, George W. Bush (189) and Bill Clinton (396). But he has surpassed any other president in the number of commutations, 1,385.

So the question now is... Will Julian Assange agree to extradition?

If Obama grants Manning clemency Assange will agree to US extradition despite clear unconstitutionality of DoJ case https://t.co/MZU30SlfGK

— WikiLeaks (@wikileaks) January 12, 2017

via Motley Fool Headlines by on Tue, 17 Jan 2017 21:20:00 GMT

via Motley Fool Headlines by on Tue, 17 Jan 2017 21:19:00 GMT

via Motley Fool Headlines by on Tue, 17 Jan 2017 21:16:00 GMT

via Motley Fool Headlines by on Tue, 17 Jan 2017 21:11:00 GMT

via Motley Fool Headlines by on Tue, 17 Jan 2017 21:04:00 GMT

via by Tyler Durden on Tue, 17 Jan 2017 21:02:18 GMT

Today's trading brought to you by the letter "B" and not by the number 20,000...

"B" is for Breaking narratives.. as the reflation trade rolls over...

"B" is for Brexit talk from Theresa May sparked the biggest surge in cable since 1993, smashing back above 1.2400...

"B" is for Banks stumbled most since the election...(despite great earnings from MS today)

"B" is for Brazil declined Saudi production cut request and hit oil prices...

"B" is for Bullion - soaring up 16 of the last 18 days (7 in a row), touching $1220 today...

"B" is for Bonds which saw yields plunge today.... (yields down 4bps to 7bps across the curve today)

Not surprising given the record short position...

And "B" is for Blood on the streets in FX land...

* * *

Year-to-date, gold is the biggest winner and The Dow back unchanged...

Small Caps end the day in the red for 2017...

Banks led markets lower...

And Banks and Energy stocks are the year's biggest losers...

VIX somehow manage to end with an 11 handle...

All the majors rallied against the greenback today but it was cable that outperformed...

Since The Fed hiked rates, bonds have rallied... "policy error"?

Are stocks ready to drop back to reality?

via by Tyler Durden on Tue, 17 Jan 2017 20:50:00 GMT

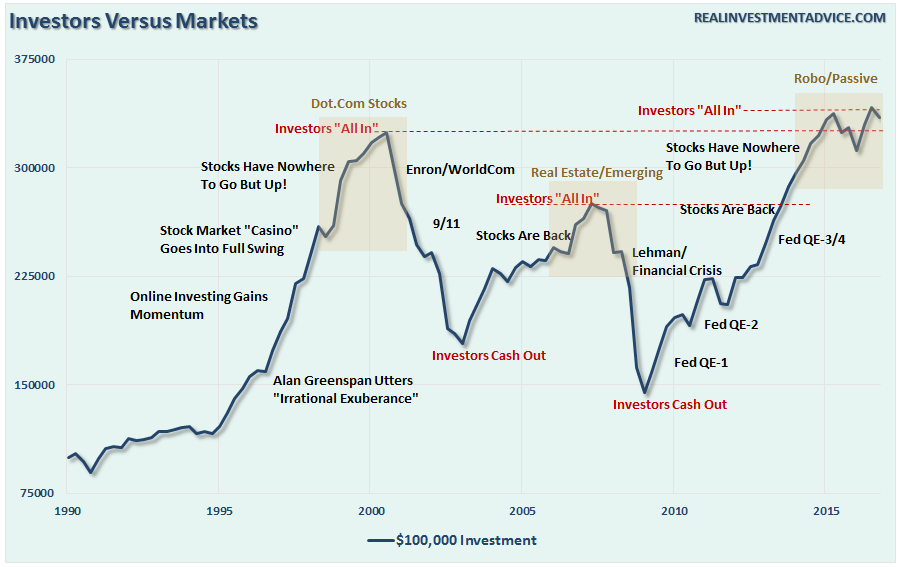

Submitted by Lance Roberts via RealInvestmentAdvice.com,

For the third time in four weeks, the market was closed on Monday due to a holiday. Not only is this week shortened by a holiday, it is also coinciding with the annual Billionaire’s convention in Davos, Switzerland and the Presidential inauguration on Friday. Increased volatility over the next couple of days will certainly not be surprising.

In this past weekend’s missive, I discussed a variety of “extremes” being registered in many areas of the market and particularly in prices. To wit:

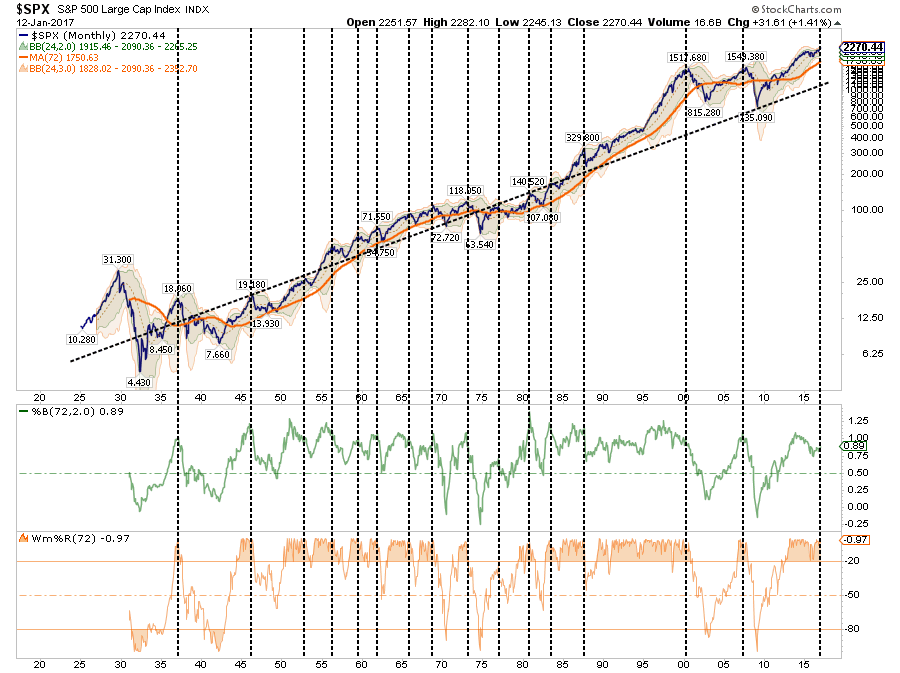

“I have often compared market prices to the equivalent of “stretching a rubber band.” Prices can only deviate so far from the long-term trend line before a mean reverting event eventually takes place. Much like a “rubber band,” prices can only be stretched so far before having to be relaxed to provide the ability to be stretched again.

The chart below shows the long-term trend in prices as compared to its underlying growth trend. The vertical dashed lines show the points where extreme overbought, extended conditions combined with extreme deviations in prices led to a mean-reverting event.”

“This is shown a bit clearer below which compares the deviation of the S&P 500 from the long-term growth trend. Currently, while only slightly below the peak of the 2000 “dot.com” bubble, the deviation is at levels that have ALWAYS coincided with a negative mean reverting event or very poor, and highly volatile, forward returns.”

I know…I know. As soon as I wrote that I could almost hear the cries of the “perma-bull” crowd exclaiming “how many times have we heard that before.”

They would be right. The problem with the majority of analysis, in my opinion, is the mismatch between long-term analysis and short-term time frames. The problem with long-term price analysis is the failure to predict short-term price changes. However, short-term analysis leads to psychological wear where analysts have spotted “Head and Shoulder” formations, “Hindenberg Omens,” and “Puppy Monkey Baby“ patterns that have failed to predict a market change.

Of course, like “crying wolf,” when these short-term patterns and long-term prognostications fail to immediately validate themselves, they are summarily dismissed as being wrong, or just “mumbo jumbo,” which often leads to unwanted outcomes.

The primary problem is the “duration mismatch” between most technical analysis, which is typically very short-term (minute, hourly, daily), and the outlook for investors which is in years.

As a portfolio manager, what is important for me is the understand the longer-term “TREND” of market prices. By looking at weekly and monthly data, the trend of prices is revealed allowing for a better match between portfolio goals and related market risks.

During “bull markets,” prices are in a steady advance with corrections to the longer-term bullish trend presenting buying opportunities. When prices become extended from the trend, such deviations provide opportunities to take profits and rebalance portfolios.

Conversely, during “bear markets,” prices are in a steady decline with corrections to the longer-term bearish trend presenting selling, hedging, and shorting opportunities. When prices become extended away from the bearish trend, such deviations should be used to take profits in short positions and portfolio hedges.

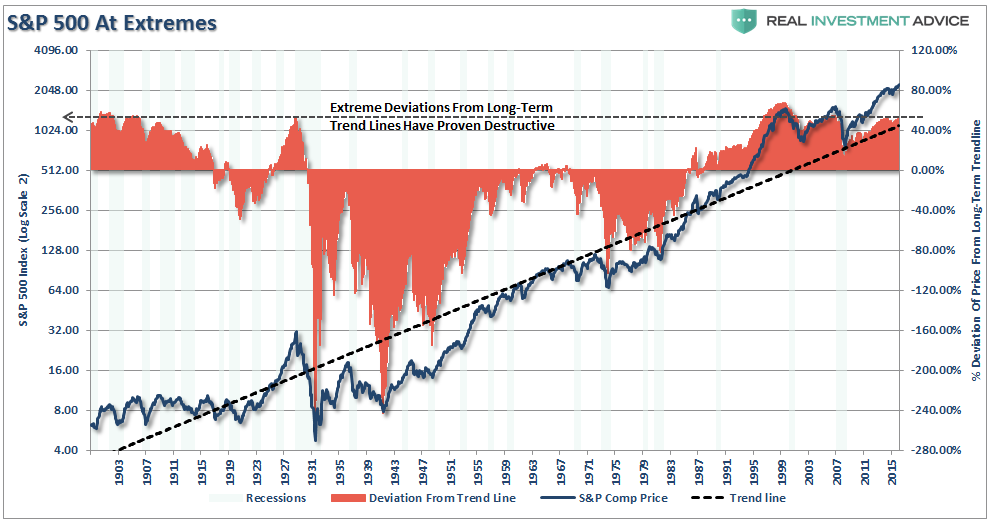

This idea is shown in the chart below.

By using a 72-week moving average, the longer-term trend of prices is more clearly revealed. As stated, corrections to the longer-term trend during bull markets were buying opportunities, whereas during bear markets they were selling/shorting opportunities.

VERY IMPORTANTLY – note that at the peak of the previous two markets the change from a bullish to a bearish trend was denoted by the following price action:

While this occurred at the beginning of 2016, it was quickly reversed following rapid intervention by global Central Banks quickly intervening with a flood of liquidity. The markets have now resumed their bullish trend currently but are pushing the limits of historical advances as noted this past weekend.

The problem ultimately comes down to psychology.

Last year, I wrote an article about the fallacies of “buy and hold” investing which received a good bit of push back from the community of advisors who tout that the only way to invest is to buy low-cost ETF’s and hold them long-term. As I penned:

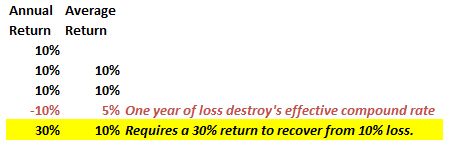

“Let’s assume an investor wants to compound their investments by 10% a year over a 5-year period.

The “power of compounding” ONLY WORKS when you do not lose money. As shown, after three straight years of 10% returns, a drawdown of just 10% cuts the average annual compound growth rate by 50%. Furthermore, it then requires a 30% return to regain the average rate of return required.

In reality, chasing returns is much less important to your long-term investment success than most believe.”

Emotions and investment decisions are very poor bedfellows. Unfortunately, the majority of investors make emotional decisions because, in reality, very FEW actually have a well-thought-out investment plan including the advisors they work with. Retail investors generally buy an off-the-shelf portfolio allocation model that is heavily weighted in equities under the illusion that over a long enough period of time they will somehow make money. Unfortunately, history has been a brutal teacher about the value of risk management.

Take a look at the chart below.

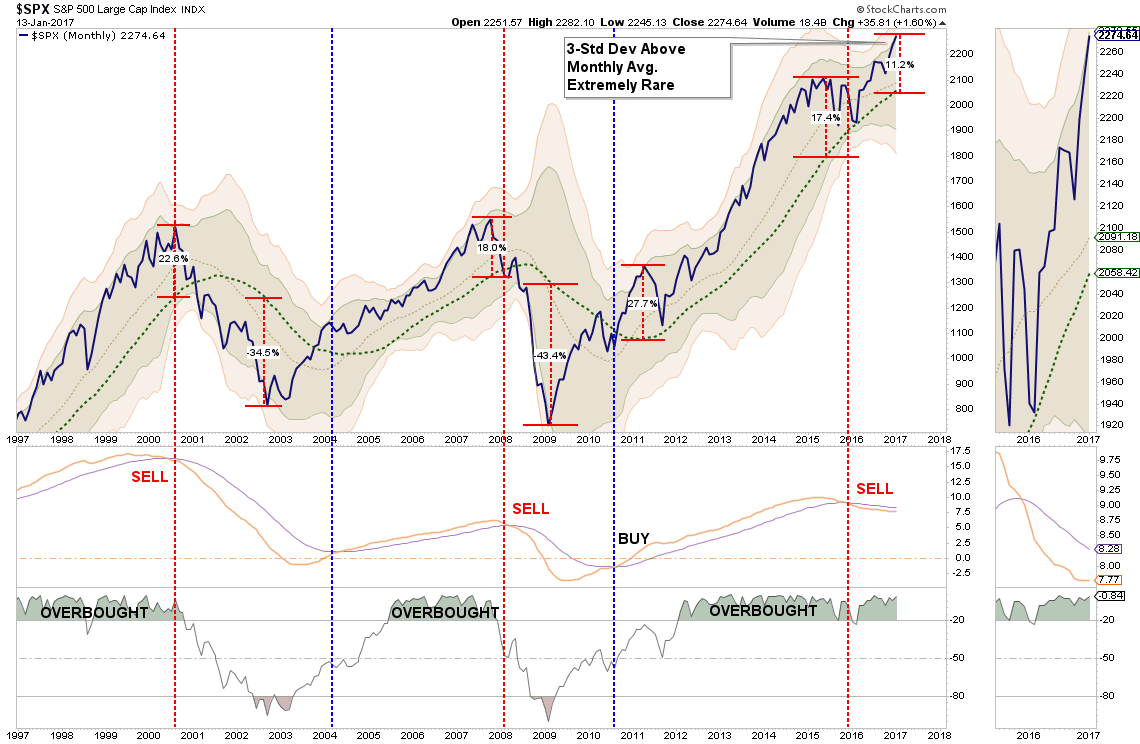

The current extension of the market above the 200-dma, combined with extremely low volatility readings and overbought conditions, have not been kind to investors over the last couple of years.

This overbullish, overextended market is also evidenced on a MONTHLY basis with prices currently pushing a rare 3-standard deviation extensions above the 3-year moving average.

Sure, this time could certainly be different. There is just a really high probability it will not be.

But such observations rarely deter individuals in the short-term as our emotionally driven “fear of missing out” and the now ingrained belief the “Fed won’t let the market fail,” blinds us to a multitude of psychological traps. These “traps” are the biggest reason for underperformance by investors who participate in the financial markets over time.

The biggest of these problems for individuals is the “herding effect” and “loss aversion.”

These two behaviors tend to function together compounding the issues of investor mistakes over time. As markets are rising, individuals are lead to believe that the current price trend will continue to last for an indefinite period. The longer the rising trend last, the more ingrained the belief becomes until the last of “holdouts” finally “buys in” as the financial markets evolve into a “euphoric state.”

As the markets decline, there is a slow realization that “this decline” is something more than a “buy the dip” opportunity. As losses mount, the anxiety of loss begins to mount until individuals seek to “avert further loss” by selling. As shown in the chart below, this behavioral trend runs counter-intuitive to the “buy low/sell high” investment rule.

Despite all of the arm waving and pounding on the table by advisors touting long-term average returns, time-in-the-market, etc., the psychological impact of loss is all too real. While “buy and hold” investing has its appeal during bullish trending markets, the “impact of loss” on individuals is a far greater emotional pull. This is why investors tend to do everything backwards by “buying high” (greed) and “selling low” (fear).

This is why managing “risk” always “wins” over the long-term by reducing the emotional pull to “do something” at precisely the wrong time. The reality of loss tends to be more than most can stomach and sentiments of “time in the market” will go mostly unheeded. This is, of course, why many of the coveted millennial investors have already rejected much of the Wall Street rhetoric after watching the devastation that wrecked their parents over the last 15 years.

You can do better.

via by Tyler Durden on Tue, 17 Jan 2017 20:48:01 GMT

Accused Florida gunman, Esteban Santiago, who is charged with opening fire at a Florida airport, killing five victims and wounding six others, told investigators that he spoke with ISIS terrorists in “jihadi chat rooms” and carried out the deadly Jan. 6 attack on behalf of ISIS, authorities said Tuesday during a bond hearing.

Speaking at a bond hearing in Florida, FBI Special Agent Michael Ferlazzo testified that Esteban Santiago did not specify whether he was acting on ISIS' orders or was inspired by the group, according to CNN.

Ferlazzo said Santiago told him that he was in touch with like-minded individuals on jihadi web forums as they plotted similar attacks. He previously admitted to carrying out the mass shooting, according to authorities cited by AA.

“At various points…he said he carried out the attack because of government mind control,” prosecutor Ricardo Del Toro said. “But he later said he did so because of [ISIS]…after participating in jihadi chat roms.”

Santiago faces multiple charges related to the Jan. 7 shootings at Fort Lauderdale-Hollywood International Airport, including using and carrying a firearm during and in relation to a crime of violence; performing an act of violence against a person at an airport serving international civil aviation that caused serious bodily injury; and causing the death of a person through the use of a firearm.

If convicted, he could face the death penalty on the last two charges. Santiago deployed to Iraq in 2010 as part of the Puerto Rico National Guard, and stayed there for a year before returning to the U.S. He reportedly suffered from mental health problems.

Santiago is being held without bond following Tuesday's hearing. He will next appear in court Jan. 30.

via Motley Fool Headlines by on Tue, 17 Jan 2017 20:43:00 GMT